30 on 30

Manufacturing Sector – Transition Briefing

Addressing cost, market access, and talent to support Ontario’s manufacturing sector

Issue

Manufacturing remains a key part of Ontario’s economy. The sector has experienced structural changes in recent decades but is still a major driver of investment, innovation, and employment in the province. The incoming government will need a strategy to support manufacturing’s competitiveness and the sector’s continued role in opportunity and prosperity in Ontario. An effective manufacturing strategy will need to tackle (1) costs, (2) market access, and (3) talent.

Overview: Manufacturing in Ontario

The manufacturing’s sector has been undergoing a transformation in recent years. This is reflected in new technologies, new processes and applications, and of course changes in employment levels and the types of employment.[1]

This transformation – including, for instance, the emergence of new, advanced manufacturing sub-sectors – is reshaping how we think about manufacturing. There is some speculation that we are experiencing a “manufacturing renaissance.”

These trends are no doubt positive. It might even lead policymakers to be complacent about Ontario manufacturing. Manufacturing GDP and exports are growing again after the punishing blow of the 2008-09 global recession. The Canadian dollar has returned to near its equilibrium level and manufacturers are busy despite the uncertainty associated with the NAFTA negotiations.

However, being complacent about Ontario manufacturing would be a mistake. Ontario firms are growing less competitive and thus missing out on the opportunities that expanding local and global economies provide. How do we know? Canadian manufacturers are losing market share at home and abroad. Our foreign competitors are taking an increasing share of new and existing customers. As a result, we are losing opportunities to create jobs and grow profits here in Ontario.

The need for reform

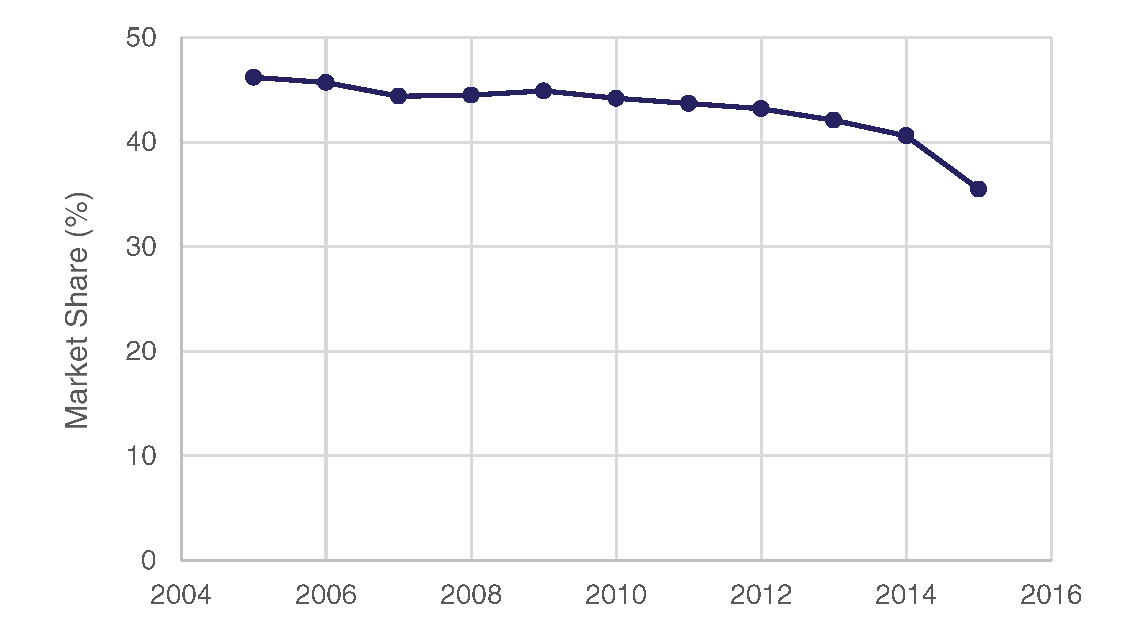

Figure 1 shows that Canadian manufacturers have been steadily losing domestic market share since 2009.

Figure 1. Canadian share of Canadian manufacturing market from 2005-2015. Source: CANSIM Table 304-0014 and Innovation, Science and Economic Development Canada and Trade Online

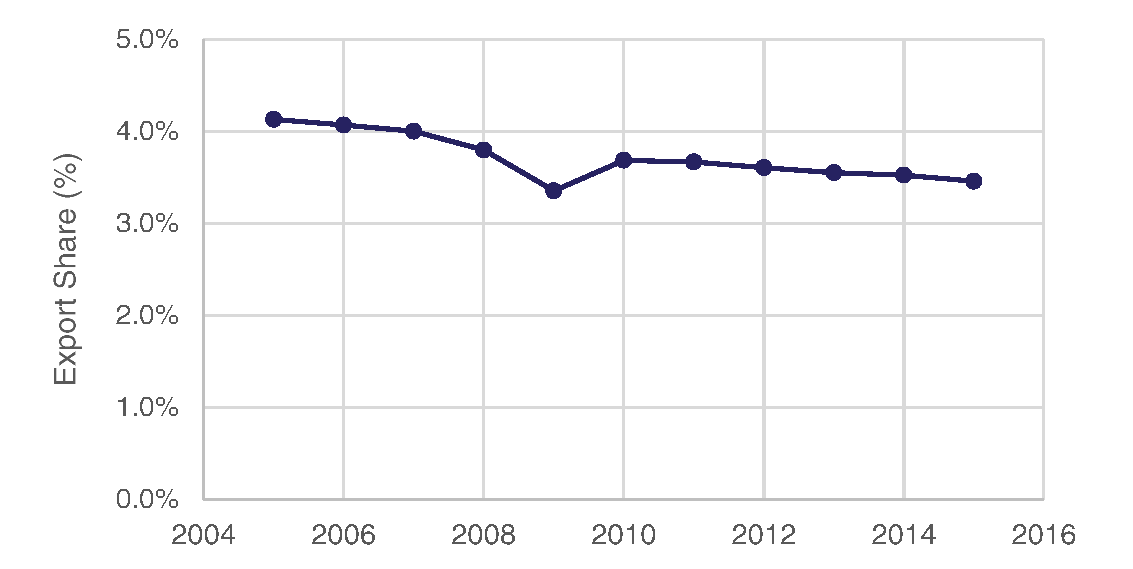

In addition, as shown on Figure 2, over the last decade Canadian manufacturing exports have accounted for a steadily declining proportion of the U.S. domestic market.

Figure 2. Canadian share of US manufacturing market. Source: OECD Bilateral Trade Database, ISIC Rev. 4

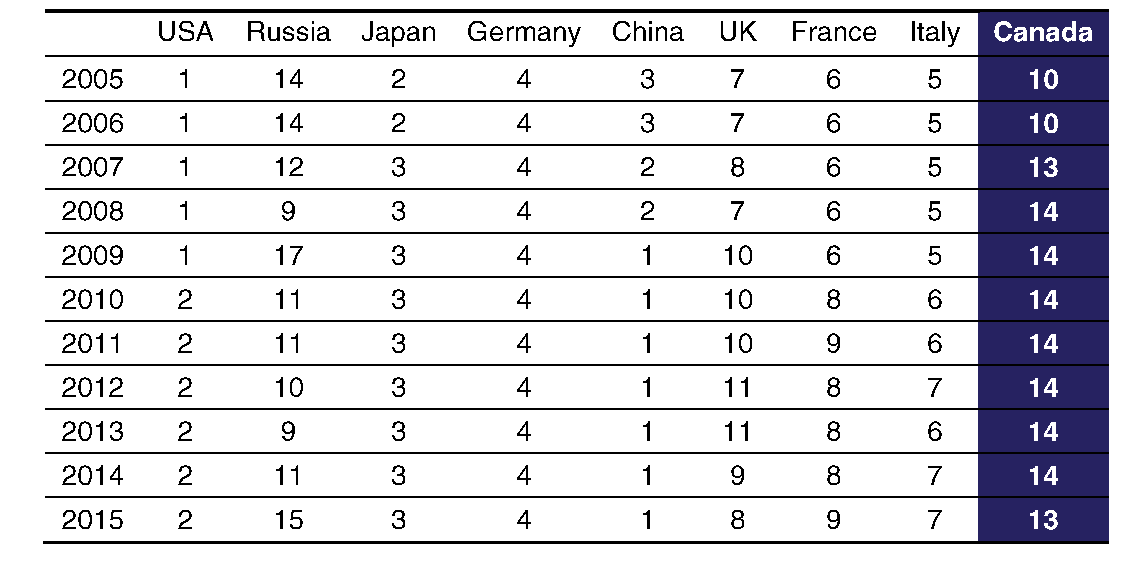

Globally, Canada’s ranking in world manufacturing has been slipping in recent years. According to UN figures (Table 1), Canada has slipped from the 10th most important manufacturer in 2005 to 13th in 2015.

Table 1. Rank in world manufacturing by country. Data Source: UN National Accounts Main Aggregates Database, uploaded January 2017, with data from 1970 to 2015.

How to move forward

What, if anything, can governments do about our declining manufacturing competitiveness? We can break the competitiveness challenge into three elements.

The first element is cost. Governments have a big impact on manufacturing costs through taxes, regulations and the cost of publicly-provided services. Canada’s highly-touted business tax advantage was largely eliminated by the Americans’ recent tax reform. We are now roughly even with the US and below a number of our competitors, especially those in emerging markets.

Governments also affect manufacturing firm costs through regulation. Every time we mandate new holidays or social-oriented mandates we make our factories less competitive. More and more, governments are forcing employers to bear the costs of social policy. What politicians do not seem to realize is that the increased costs from these policies reduce jobs and profits and ultimately make our firms less competitive.

A second element of the competitiveness challenge is market access. Ontario manufacturers need easy access to domestic and foreign markets. One part of promoting market access for our firms requires the negotiation (or re-negotiation of trade agreements (internal trade, NAFTA, CETA, TPP and most recently, the Pacific Alliance and Mercosur). Another part requires modern infrastructure, i.e., ensuring that firms can access markets with efficient road, rail, air and border infrastructure. The federal government leads on international trade negotiations, but infrastructure is a key provincial responsibility. A considerable share of Ontario’s 13-year, $190 billion infrastructure spending should be dedicated to market access infrastructure such as highways, bridges, and shipping-related assets.

A third element of competitiveness challenge is talent. Ontario manufacturers need talented workers with up-to-date skills to compete in the increasingly complex world of advanced manufacturing. Part of the responsibility for developing skills rests with workers and students themselves and another part rests with employers. However, government policies and post-secondary institutions also have an important role to play.

In sum, regardless of which political party forms government after the upcoming general election, they will need to confront the serious competitiveness challenge that Ontario manufacturing is facing. While firms themselves must take the lead, governments have an important role to play in addressing all three elements of the competitiveness challenge.

Specifically, governments need to address the tax and regulatory burden faced by firms. They need to promote market access through trade agreements and trade and investment missions, and ensuring that efficient transportation and border infrastructure is available to bring our goods to markets. Finally, they need to align government policies, programs and institutions to help firms, workers and students build the skills they need to compete in the world of advanced manufacturing.

Paul Boothe, David Moloney and Alister Smith are with the Trillium Network for Advanced Manufacturing, a non-profit organization dedicated to supporting the growth of Ontario manufacturing