Policy Papers

The 2023 Ontario Budget: Consistent Industrial Strategies and Traditional Spending Needs Amid Improved Fiscal Circumstances

This briefing summarizes the key economic, financial, and strategic policy aspects of the 2023 Ontario Budget tabled on March 23.

Overview

This Ontario 360 briefing note summarizes and comments on the key economic, financial, and strategic policy aspects of the 2023 Ontario Budget tabled on March 23.

Entitled “Building A Strong Ontario”, the budget from a policy point-of-view was marked by a focus on the manufacturing sector and skilled trades. From a fiscal standpoint, a massive increase in projected revenues funded a substantial increase in health care funding and significant improvements to the fiscal outlook.

Economic Policy

The centrepiece of the government’s economic policy was a clear and sensible cluster strategy encompassing manufacturing, electric vehicles, mining, critical minerals, and the Ring of Fire. This strategy builds on several of the province’s fundamental economic strengths. It is already paying dividends based on the substantial new private-sector investments announced in electric vehicle-related manufacturing in the province. A new “Made in Ontario” manufacturing investment tax credit will support that sector broadly while there was some new funding committed for critical minerals and mining exploration programs. There were some bold words regarding jobs in the manufacturing sector and progress on the Ring of Fire that may come back to haunt the government, but only time will tell.

Infrastructure investments are the other pillar of the government’s plan to build the Ontario economy. The capital plan devotes more than $184 billion to public infrastructure over the next ten years. It would take a keen-eyed reader to discern how much of the higher amount than announced in the 2022 Ontario Budget ($158 billion over 10 years) is devoted to new projects versus representing higher costs related to previous commitments. Regardless, it is a sizeable and ambitious plan. There is a strong emphasis on improving practices to build highways, transit, and community infrastructure projects better and faster. This emphasis is welcome, given the tradition of projects taking much longer than planned.

The Ford government is very supportive of the manufacturing, mining and construction sectors. What about the rest of the economy? These three sectors represented 24 per cent of provincial private-sector employment in 2022. There may be a strong policy case for prioritizing these sectors (including pre-existing advantages or economic spillovers) but the budget does not provide a framework for assessing its sectoral priorities. Ontario has many other sectors with strong underlying fundamentals and solid growth records, including the finance, cultural/creative and professional, scientific and technical services sectors contributing to the province’s economic prosperity. If the government is going to preference particular sectors, it should set out a strategy that better roots its policy choices. The forthcoming long-range assessment of Ontario’s economic and fiscal environment required by the Fiscal Sustainability, Transparency and Accountability Act 2019 would be an ideal opportunity to outline such an economic strategy.

One of the intriguing commitments in the Budget was the announced review of Ontario’s tax system that would prioritize competitiveness and long‐term growth in the province. It will be interesting to hear more about how the province plans to do this including whether such a review is carried out internally or through some external process. Hopefully, it will lead to some ideas more creative than the usual advice to simply lower corporate income tax rates which failed to yield the expected economic benefits last time Canadian governments followed that path.

While there is limited progress on the climate change file in the Budget, there are few encouraging signs that the government is nudging itself towards recognizing that a greener future is a significant economic opportunity. For example, the strategy around electric vehicles and critical minerals is an opportunity for the province to transition towards the cleaner economy of the future. The budget materials also correctly recognize the economic benefits of Ontario’s clean energy supply, even if it does not recognize that this is mainly due to some courageous and financially costly policy decisions of the preceding Liberal government. Finally, the Budget also identifies the benefits of the province’s Emissions Performance Standards (EPS) program as an alternative to the federal Output‐Based Pricing System (OBPS) on industrial emissions. The EPS is essentially a cap-and-trade system applied to industrial emissions, so the province has embraced carbon pricing in some parts of the economy, which is encouraging even if it might have been done purely as a defensive response to the federal carbon backstop policies.

The Budget continues the government’s already substantial commitment to promoting skilled trades. Additional funding was provided for expanding training centers, the Ontario Immigrant Nominee Program and other skills development programming. The importance of increasing the skilled trades labour force is supported by a Buildforce Canada study, which shows that Ontario will need about 72,000 additional construction workers by 2027 to help deliver the province’s ambitious capital plan, including getting 1.5 million homes built by 2031.

The Budget has very little in it regarding labour force skills more broadly. New manufacturers, mines and construction projects will need more than skilled trades. They will need engineers, architects, planners, lawyers, accountants, financiers, safety officers and human resources professionals. In other words, they will need college and university graduates. The economic importance of post-secondary education is demonstrated by a recent survey of employers conducted by the Business Council of Canada that indicates that the most in-demand skills over the next three years will be those typically provided though a college or university program. The Budget had little to say about post-secondary education policy, which may be a good thing given the potential for further harm. On a positive note, there is a bit of recognition of the value of the post secondary education sector in the Budget, including some modest investments to support health human resources, research and innovation.

Affordability

The 2023 Budget included one notable measure related to improving affordability: a commitment to expand the province’s Guaranteed Annual Income Supplement (GAINS) program. The expansion will take effect on July 2024 with a commitment that about 100,000 more seniors will be eligible for the program. This enhancement was not directly connected to high consumer price inflation rates. GAINS targets income supports to low-income seniors, and as such, this measure will not reach a broader population of low-income people who may be struggling in the face of higher costs of food and rent. This measure is also not a timely response to high consumer price inflation rates, which are projected to be back to around 2 per cent based on the Budget economic forecast by the time the enhancement takes effect. The Budget does not describe the new program parameters or why it is waiting until 2024 to implement it.

The Budget includes an extensive narrative on past affordability measures implemented by the government. Examples include relief from automobile licence renewal fees, lower gasoline and fuel taxes and keeping down the cost of electricity. Indeed, a lot has already been done, and it must be the government’s view that it has done enough or that further measures may risk contributing to inflationary pressures.

Looking ahead, there will be keen interest in seeing how the government accounts for this period of high inflation when it comes time to resetting parameters for social programs such as Ontario Works.

There was little incremental action in the Budget to address housing affordability. The government introduced a broad range of measures in November 2022 with the More Homes Built Faster Act. There was a call on the federal government to provide sales tax relief to support new housing and rental development. It is unclear why the province feels a measure that would alleviate a small portion of construction costs would have a meaningful impact on housing construction and supply.

The forecast for housing starts contained in the Budget has been used as evidence that the government’s goal of 1.5 million new housing units by 2031 was unrealistic. The province’s housing supply target is certainly incredibly ambitious. However, a cautious housing start projection based on private sector forecasts should not be interpreted as an early admission of failure. It is common practice that Budget economic forecasts do not incorporate the potential behavioural impacts of government policy. The private sector economic forecasts that form the basis of the government’s planning assumptions usually only attempt to incorporate new government policy once they have begun to have a material impact. Furthermore, reflecting the positive economic impact of a new policy in the economic forecast would not be prudent and could lead to overly aggressive economic and revenue growth projections.

Health Care

The Budget included a significant increase in funding allocated to health care, boosting its allocation to the sector by $15.3 billion (6.4 per cent) over the next three years compared to amounts planned a year ago. The planned spending increase includes $4.4 billion in new federal funding and $10.9 billion allocated from provincial coffers. The increased allocation is devoted to implementing a broad range of initiatives, including those outlined in “Your Health: A Plan for Connected and Convenient Care,” announced by the Minister of Health in February 2022. In addition, the Budget recognized and provided new funding to the health care areas of greatest need, including primary care, wait times backlog, long-term care and health human resources.

It is good news that the government has a plan to address health care challenges and has allocated significant funding towards that goal.

There was also recognition of the importance of addressing health human resources shortages. The Budget noted that over 60,000 new nurses and nearly 8,000 new physicians had begun work in Ontario since 2018. The net change in the number of nurses and physicians over that period, taking into account departures through retirements and other reasons, would be an an equally interesting fact. There were several initiatives in the Budget to encourage both the supply and employment of health care workers, including expanded enrolment for nursing programs, incentives for nurses to remain in the workforce and getting foreign-trained doctors certified in the province. Only time will tell if the plan and funding are sufficient. The main concern is whether the province can address health human resource challenges without a new compensation framework. As such, the government still has not delivered a way to reset its approach to compensation that is appropriate and necessary given the seismic shifts in health care, the economy and government finances since Bill 124 was introduced and passed in 2019.

Economy

The Budget economic planning assumptions indicate minimal economic growth in 2023, with real Gross Domestic Product (GDP) increasing by a minuscule 0.2 per cent. This annual growth rate implies at least one quarter with a very modest reduction in real GDP, but not necessarily a recession. Real GDP growth is expected to rebound over the planning period, rising to 1.3 per cent in 2024 and 2.5 per cent in 2025. The economic planning assumptions were calibrated to an average among private sector forecasts available in January with a 0.1 percentage point reduction for prudence. This amount of prudence is consistent with past practice in the years prior to COVID-19. A few private sector forecasts updated since January have been edging down slightly, but there are no material changes to date.

The outlook for CPI, likely also benchmarked to private sector views available in January, indicates a steady decline in annualized inflation from 6.8 per cent in 2022 to 3.6 in 2023 and back to central bank targets of around 2.0 per cent afterward. The forecast of an annual increase of 3.6 per cent indicates that CPI inflation is expected to slow throughout 2023, likely declining to within a range of 2 to 3 per cent towards the end of the year. The sharp reduction in the February 2023 CPI released a few days before the Budget suggests that the risks are balanced towards a slower price inflation rate this year than included in the Budget.

Key risks to the economic growth outlook identified in the Budget are largely downside, including the potential for price inflation to persist, further tightening of monetary policy, slower US growth and continued geopolitical tension and conflict. The reopening of the China economy is an upside risk to GDP growth and commodity prices. The Budget would have been finalized before the recent turbulence in the US and global banking sectors, an emerging risk for US economic growth and an example of the benefits of adopting prudent economic planning assumptions.

Fiscal Plan

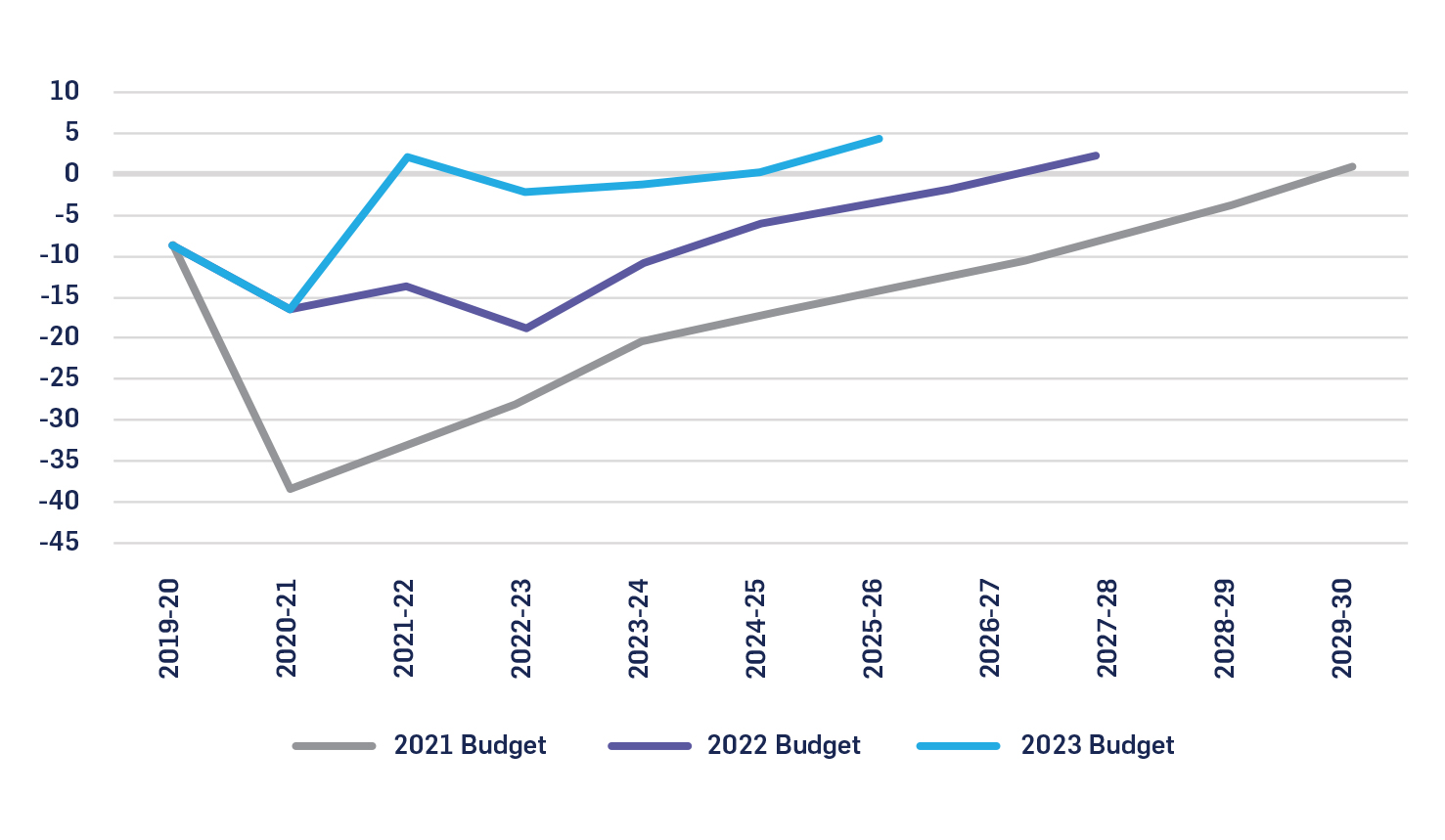

The 2023 Budget included yet another remarkable improvement in the province’s finances. Officially, the province is planning for slight deficits in 2022-23 (-$2.2 billion) and 2023-24 (-$1.3 billion) with a return to balanced budgets in 2024-25 (+$0.2B) and continuing into 2025-26 ($4.4B). Those two deficits are inconsequential when considered in the context of a $1 trillion provincial economy or government revenues and expenses of $200 billion. From an economic perspective, the budget is essentially balanced every year.

The estimated deficit of $2.2 billion in 2023-23 is very cautious. It includes $1.75 billion in contingency funds available to offset additional expenses that may materialize before the end of the fiscal year. It is unusual to carry significant contingencies so late in the fiscal year. Also, lower expenses and higher revenues will likely be recorded at year-end, suggesting the Budget will be balanced in 2022-23.

There are also $6.3 billion in extraordinary expenses recorded in 2022-23 for costs associated with ongoing land and land‐related claims with Indigenous communities. The total allowance increased by $1.25 billion since the 2022-23 Third Quarter Finances. It will be interesting to hear more about these claims and how the Auditor General will view expensing these amounts.

The fiscal outlook for 2023-24 to 2024-26 also appears prudent. As discussed above, a modest amount of prudence is reflected in the economic planning assumptions that underly the fiscal projections. Also, given the unprecedented revenue windfall of the past few years, it is not easy to assess how prudent the revenue outlook may be. An expense contingency fund of $4.0B billion in 2023-24 is enormous compared to pre-COVID norms. The size of the contingency fund for 2024-25 and 2025-26 is not disclosed as usual, but the reasonably flat “Other Programs” sector expense line suggests it is comparable to 2022-23. A much larger than usual fiscal reserve is included in 2024-25 ($2 billion) and 2025-26 ($4 billion).

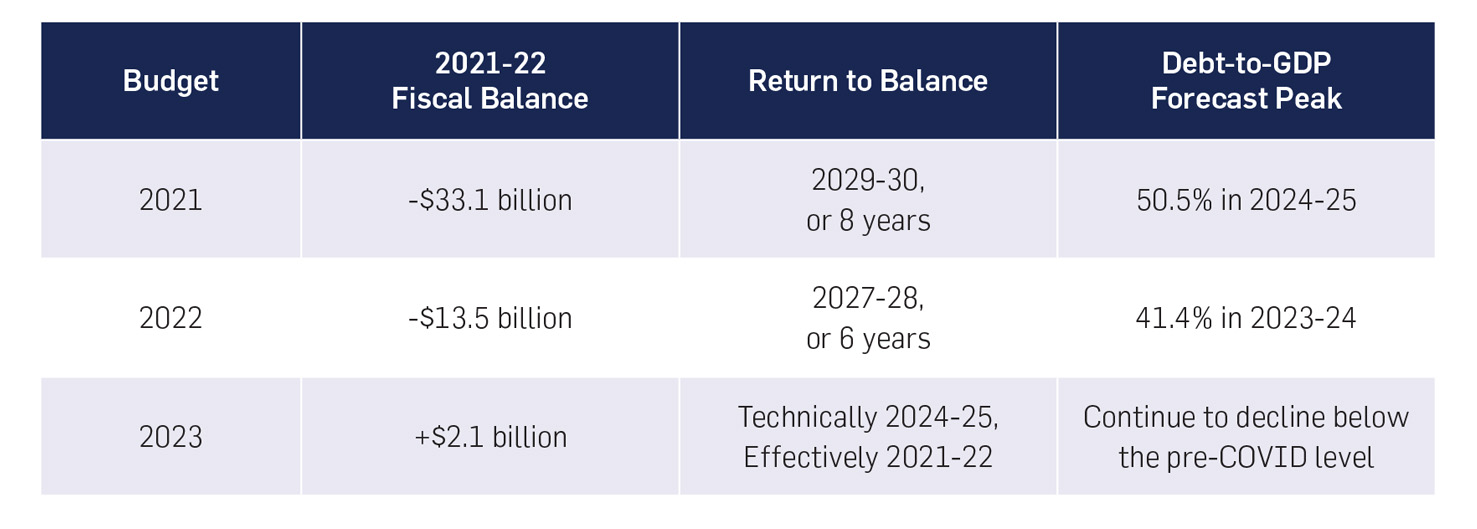

The current fiscal track represents a significant improvement from the 2022 Budget, with the previously projected deficits essentially eliminated and a substantially lower debt burden. Even more remarkable is to consider how dramatically things have changed since the 2021 Budget was tabled just two years ago, when a record-high deficit of $33 billion was expected in 2021-22, a long eight-year path to a balanced budget projected and for debt to GDP to peak at a whopping 50.5 per cent of GDP. How much things have changed in two years!

Table 1: Evolution of Ontario’s Fiscal Outlook

Figure 1: Ontario Deficit Projections ($billions)

Brian Lewis is a senior fellow and lecturer at the Munk School of Global Affairs and Public Policy at the University of Toronto. He is the former chief economist at the Province of Ontario.