Policy Papers

Ontario Budgeting: Darkening Clouds Raise Stakes for Fall Economic Statement

Normally, the fall economic statement in the second year of a government’s mandate would be low-key. These are not normal times. Political, financial, and economic challenges have combined to raise the stakes. Furthermore, unemployment and consumer price inflation have risen recently, indicating times are becoming more challenging for many Ontario households.

Introduction

For most Canadians, autumn is when the weather turns colder, the leaves turn colour, and attention starts to turn towards the year-end holiday season. For Canadians interested in government finances, it is also “Fall Economic Statement” season. Most senior governments in Canada have a tradition of delivering an economic and financial update in the fall because this is roughly halfway through the April 1 to March 31 fiscal year. For Ontario, the Fiscal Sustainability, Transparency and Accountability Act requires a mid-year review by mid-November. This year, the Ontario government will release its annual Ontario Economic and Fiscal Review, more commonly referred to as the Fall Economic Statement, on Thursday, November 2, 2023.

Normally, the fall economic statement in the second year of a government’s mandate would be low-key. With the previous election out of the way and the next one well into the future, political attention would be at an electoral cycle low point. As such, this fall economic statement at Queen’s Park would typically be a low-stakes, low-profile affair.

These are not normal times. Political, financial, and economic challenges have combined to raise the stakes. Politically, the Greenbelt scandal has damaged the government’s credibility and popularity. Financially, the 2022-23 fiscal year ended with a much higher deficit than estimated in the spring 2023 Budget and represents a downside risk to the fiscal plan for 2023-24 and beyond. Economic growth prospects for 2023 have improved since the Budget, but recession risks persist, and growth projections for 2024 have been coming down. Furthermore, unemployment and consumer price inflation have risen recently, indicating times are becoming more challenging for many Ontario households.

Recommended Approach for the 2023 Ontario Economic Outlook and Fiscal Review

In the presence of these darkening clouds, some perspective is offered here on an appropriate approach towards the 2023 Ontario Economic Outlook and Fiscal Review.

The overriding advice is to focus on an updated assessment of the economic and financial outlook. That is to say, the emphasis of the fall economic statement should be an update of the government’s economic and fiscal projections. Current economic circumstances do not warrant a big bang “mini-Budget” kind of fall economic statement including costly spending or tax changes. Substantial new expenditures or tax cuts can be appealing from a political perspective, but this isn’t recommended at this point in the economic and fiscal cycle. From an economic perspective, fiscal expansion would result in further upward pressure on prices, undermining the Bank of Canada’s efforts to bring down inflation, a task that remains challenging. Protecting provincial finances should be the priority, given that these have worsened since March’s Budget based on the higher deficit in 2022-23 revealed in the 2022-23 Public Accounts of Ontario.

From a financial perspective, the advice is to hold to the fiscal balance outlook delivered in the 2023 Ontario Budget. It is too early to say for sure that the fiscal plan is off track in 2023-24 and for future years. A lot can change between now and the 2024 Budget, which would be the appropriate time to reconsider (and possibly adjust) the fiscal plan. At the same time, the government should be transparent about the impact of developments in the six months since the 2023 Ontario Budget. These impacts would include the implications of lower 2022-23 Personal Income Tax revenues, the cost of provincial HST relief for new rental housing construction, and the government’s decision to cover one-third of the price tag to subsidize multi-billion-dollar investments by Stellantis and Volkswagen.

The government should continue to be prudent in its economic and fiscal outlook. Several factors tilt risks towards the downside for Ontario’s economy and finances based on developments since the 2023 Ontario Budget. These include ongoing geopolitical risks, the previously-mentioned significant shortfall in 2022-23 Personal Income Tax revenues, which indicates that the bonanza of the past few years is over, possible downward adjustments to Corporate Income Tax and Land Transfer Tax revenues due to recent financial and housing market developments, and higher CPI inflation and collective bargaining, which could be a pressure on future expenditures.

The government should also deliver an economic update accountable to the province’s citizens. The commitment to providing the update on November 2 – well before the November 15 deadline – is a positive step in this regard. Clear transparency about the previously mentioned risks to the fiscal plan is also essential. The government should use this assessment of provincial finances to set the stage strategically for consultations to inform the 2024 Budget, which would be the right time for enacting any changes in fiscal policy.

Being seen as effective managers of the province’s finances can also be a helpful step towards recovering credibility in the context of the Greenbelt scandal. Improving confidence is a long-term strategy, not a short-term fix.

The government should continue to provide progress updates on key policy areas. Housing and health care are of prevailing importance to Ontarians. Some reasonable and realistic targets for housing supply over the next three years would be appropriate. The results achieved in addressing the health sector human resources shortage are similarly useful. A report on new developments arising from the province’s industrial policies would also be helpful.

The fall economic statement should more broadly include an appropriate focus on issues that have potentially significant implications for the province’s finances, such as any new developments on further potential costs related to Bill 124 (which has capped public sector collectively bargained pay raises) or efforts to contain costs in the future, considering prevailing high inflation rates.

The government should also provide further information on the review of the provincial tax system outlined in the 2023 Budget. The tax system merits a thorough review, given the potential to enhance efficiency and address inequity. The fall economic statement would be an opportunity to signal future direction on the review. The government could leverage the annual tax expenditure report to inform this discussion further.

Finally, the Ontario government should use the fall economic statement to commit to delivering a comprehensive economic strategy for the province. There is a legislative requirement for the government to provide a long-range assessment of Ontario’s economic and fiscal environment within two years after the most recent general election – by June 2, 2024. The government could go further towards a strategy that would guide economic policy priorities for the foreseeable future.

2022-23 Financial Results Below Expectations

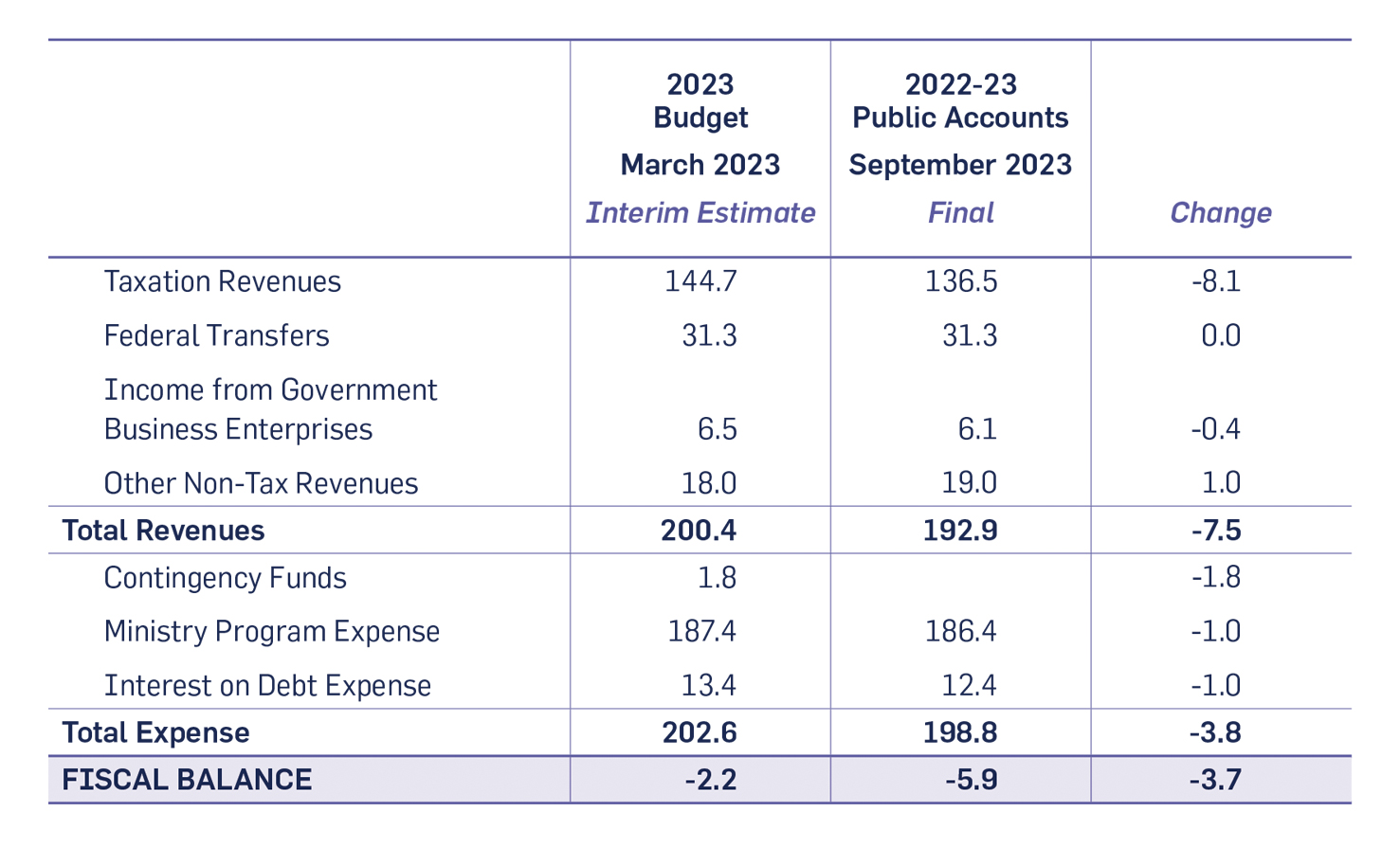

The most significant financial development since the 2023 Ontario Budget was the release of the 2022-23 Public Accounts of Ontario. The good news was that the document confirmed a much smaller deficit (-$5.9B) than planned in the April 2022 Budget (-$19.9B). The not-so-good news was that the province returned to a fiscal deficit following a modest surplus (+$2.0B) in the previous year. The clearly bad news was that the deficit was significantly larger than estimated in the March 2023 Budget (-$2.2B). This was quite surprising given the prudence embedded in the interim estimate and the historical tendency for financial results to improve when finalized in Public Accounts.

As summarized in Table 1 below, the higher deficit than expected last spring was due primarily to significantly lower taxation revenues partially offset by higher non-tax revenues, drawing down contingency funds and lower expenses.

2022-23 Ontario Financial Results

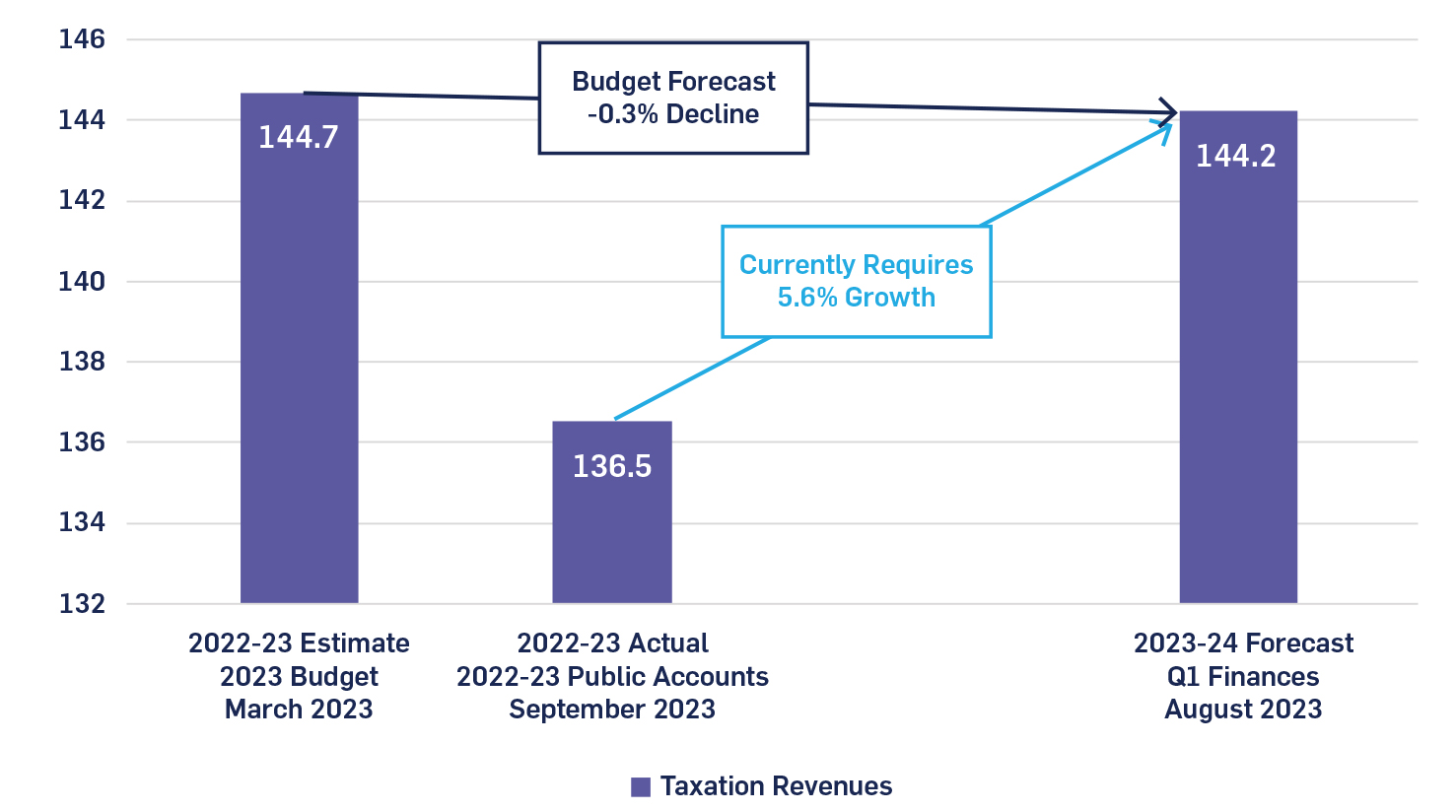

The lower taxation revenue for 2022-23 represents a downside risk to the revenue forecast for 2023-24 and beyond. Based on the lower taxation revenues earned in 2022-23, a growth rate of 5.6% is needed to achieve the forecast for 2023-24 because the year-over-year baseline has changed. This growth rate would be substantially higher than the -0.3% year-over-year decline projected for 2023-24 in the 2023 Budget. It would also require more robust growth than indicated by recent private sector economic forecasts calling for 2023 nominal GDP growth averaging about 3.5 per cent.

2023-24 Taxation Revenue Forecast ($ billions)

It is possible that revenues will still reach the 2023 Budget forecast. Some of the weaknesses in 2022-23 may have been one-time. Higher-than-expected economic growth and inflation in 2023 may fuel more robust revenue growth this year. The processing of tax returns after Public Accounts – notably 2022 Corporate Income Tax amounts – may lift this year’s numbers. There is also some potential for higher amounts from inflation-fueled Harmonized Sales Tax revenue earned during 2022 and 2023. However, as mentioned, the finalized revenue results from 2022-23 still, on balance, represent a downside risk to this year’s outlook. Even if there is a revenue shortfall in 2023-24, achieving the government’s budget projection could still be within reach due to prudence built into the plan, such as $3.2 billion in contingency funds and $1 billion fiscal reserve reported in the 2023-24 First Quarter Ontario Finances.

Also notable in the Public Accounts were significant expenses – estimated at around $8.75B[i] – recognized for contingent liabilities such as Treaty rights, Aboriginal rights, and other claims against the Crown. The events that correspond to these liabilities occurred before 2022-23, indicating that the underlying finances during the year were much better than those characterized by the deficit. Excluding the effect of contingent liability expenses, there would have been a fiscal surplus in 2022-23 of roughly $3 billion.

Mixed Economic Developments

The provincial economy has been sending mixed signals since the 2023 Ontario Budget. Economic growth prospects for 2023 have improved. However, unemployment has been rising, consumer price inflation has accelerated, and growth expectations for 2024 are down.

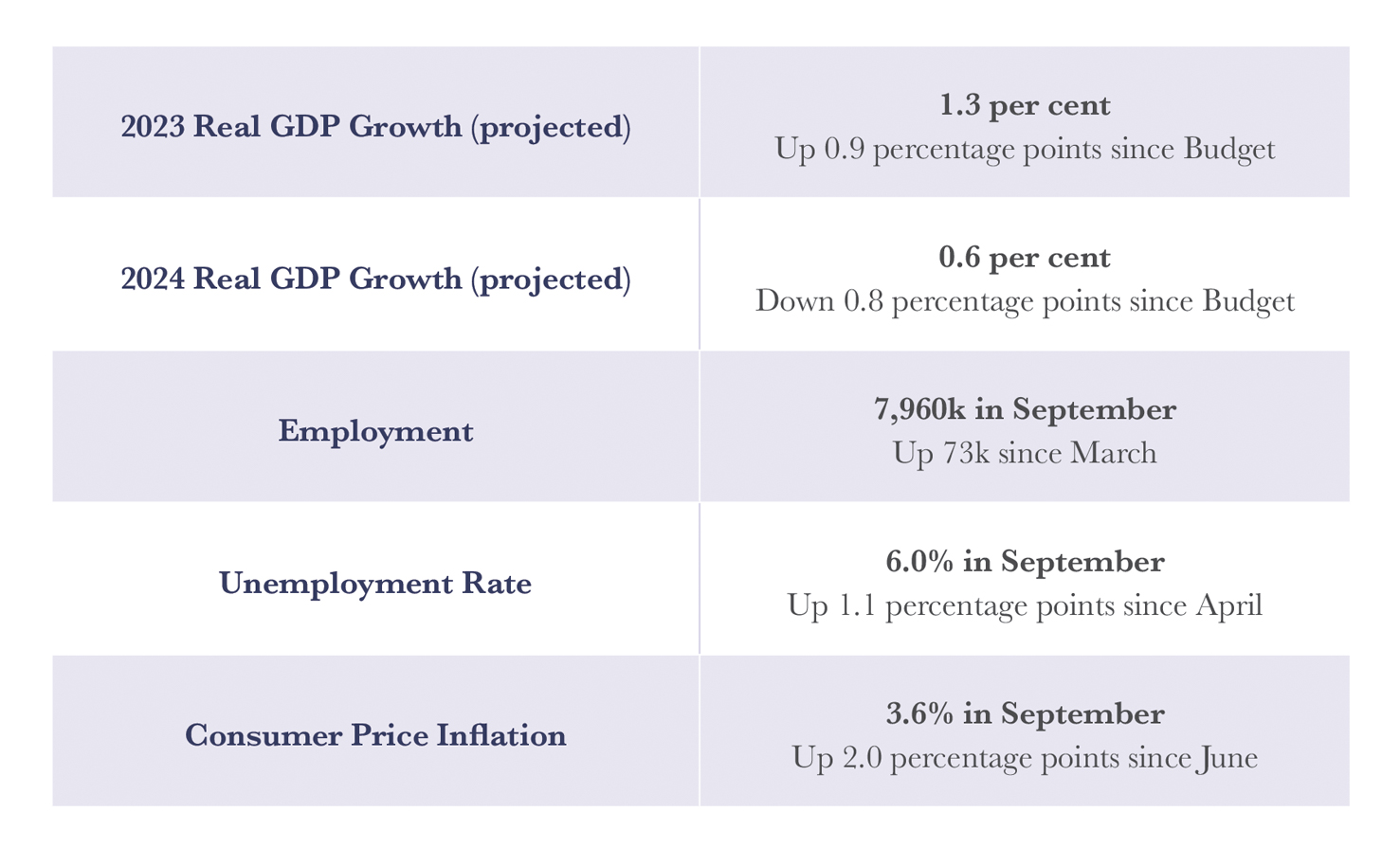

Real Gross Domestic Product (GDP) edged up 0.2 per cent in the April to June quarter, following 0.8 per cent growth during the previous quarter. Growth during the first half of the year was better than expected at the time of the 2023 Budget. As a result, private-sector economic analysts have increased growth forecasts for 2023. However, rising geopolitical risks, higher interest rates and a slowing global economy have led to lower growth forecasts for 2024. The outcome of the recent economic forecasts is increased growth in 2023 and a comparable decline in the 2024 outlook. For example, a recent BMO Capital Markets forecast projected 1.1 per cent real GDP growth for 2023 and just 0.5 per cent for 2024. In January, the projection was for 0.2 per cent in 2023 and 1.2 per cent growth in 2024.

There are varying views on the likelihood of a recession in late 2023, but the prevailing sentiment is that if there is a recession, it would be very mild. The Ontario economy may be slipping into a technical recession now, in fact, which is defined widely as two successive quarters of flat or negative growth. The University of Toronto Policy and Economic Analysis Program forecast prepared in August calls for very slight declines in real GDP during 2023Q3 and 2023Q4.

There is also mixed news regarding provincial labour markets. Employment in September was up by 73,000 net jobs (+0.9%) compared to March, as gains in three of the past six months more than offset slight declines in May, July and August. The unemployment rate has been rising steadily, and at 6.0% in September, it is up from 4.9% as recently as April 2023. While this is still low from a historical perspective, it indicates that job openings have not kept up with the rising number of job seekers in recent months.

Consumer price inflation has been mostly accelerating in recent months, rising to 3.8 per cent year-over-year in August, up from 2.6% two months ago and easing slightly to 3.6 per cent in September. This represented a significant reversal in the trend toward lower CPI inflation widely expected at the time of the 2023 Ontario Budget. Headline CPI inflation rebounded primarily because gasoline prices were up, reversing their steady and significant year-over-year declines since February, while the prices of food and shelter (+5.5% and +4.9% y/y, respectively, in September) continued to rise. Higher CPI inflation, specifically the rising cost of food and shelter, is a significant concern to citizens and a more considerable challenge for low-income households. The recent increase in CPI inflation also raises the possibility of further interest rate increases by the Bank of Canada, adding financial pressure on Canadian businesses and households.

Recent Economic Indicators

Sources: Real GDP projections are author calculations based on publicly available economic forecasts as of October 15, 2023. Other figures from Statistics Canada.

Brian Lewis is a senior fellow and lecturer at the Munk School of Global Affairs and Public Policy at the University of Toronto. He is the former chief economist at the Province of Ontario.

For more information about Ontario 360 and its objectives contact:

Sean Speer

Project Co-Director

[email protected]

Drew Fagan

Project Co-Director

[email protected]

on360.ca