Policy Papers

Critical Minerals: Making the Most of Ontario’s Big Opportunity

This paper sets out the geopolitical and domestic context for Ontario’s recent Critical Minerals Strategy including the huge economic and environmental opportunities. It also outlines the key challenges to greater progress in critical minerals and sets out eight concrete recommendations to make the most of Ontario’s big critical minerals opportunity.

Introduction

Last March, the Ontario government released a five-year Critical Minerals Strategy to leverage the province’s mineral strengths to increase investment and employment in the mining sector, boost domestic manufacturing, and make progress on climate change.

The dynamics around critical minerals have only heightened in the months since the strategy’s release. The geopolitical landscape – including Russia’s invasion of Ukraine and the subsequent energy crisis in Europe as well as the growing trend of U.S.-China decoupling – is a major factor. But so is Canada’s own climate goals – including the federal government’s electric vehicle mandate that 100 percent of new sales must be electric by 2035.

Ontario’s Critical Minerals Strategy is a good step. But as outlined in this paper, there are further policy actions that ought to be taken in order to address the key challenges impeding greater progress on the development and deployment of critical minerals in the name of supply chain resiliency and climate progress. In particular, the main challenges to the government’s strategy include: labour shortages, regulatory delays, relationships with First Nations communities, and mid-stream capacity development.

This paper sets out the geopolitical and domestic context for Ontario’s Critical Minerals Strategy including the huge economic and environmental opportunities for the province. It then outlines the key challenges to greater progress in critical minerals and sets out eight concrete recommendations to make the most of Ontario’s big critical minerals opportunity.

Geopolitical Landscape

The demand for critical minerals is growing rapidly as the world shifts towards a low-carbon economy. Renewable energy systems, electric vehicles (EVs), and digital devices all rely heavily on critical minerals like lithium, cobalt, nickel, and other rare earth elements. Forecasts suggest that to match the expected demand of minerals like cobalt, a 500% increase supply production will be needed by 2050. Other minerals like lithium and graphite could see demand increasing by 4000% over that same period. This surge in demand is propelled by several factors, predominantly the impetus to mitigate dependence on fossil fuels and the trend towards digitization and high-tech manufacturing worldwide.

It is well-established that certain regions of the world have a more significant abundance of critical mineral resources than others. Similarly, mining and processing operations are more concentrated in specific areas. For instance, Australia accounts for over 50% of the world’s lithium production, while the Democratic Republic of Congo (DRC) holds nearly half of global cobalt reserves. Indonesia contributes nearly 40% of global nickel output, and China dominates the world’s graphite supply with 79% of market share. One of the foremost challenges faced by policymakers is, therefore, to ensure a reliable and sustainable supply of critical minerals while also addressing sustainability concerns and promoting responsible extraction practices.

The mining industry has historically been known for exploitative practices, with notable examples including the use of child labour for cobalt mining in the DRC, the carbon-intensive conversion of Indonesian Class 2 nickel into battery-grade Class 1 nickel, and the water-intensive extraction of lithium in Chile that has caused arid conditions and harm to the surrounding ecosystem. With recognition that the level of production for these minerals must increase greatly in coming years, it will be imperative too that policymakers prioritize responsible extraction practices and address social, environmental, and governance (ESG) considerations in the production of critical minerals.

In addition to exposure of critical mineral supply chains to vulnerabilities arising from political instability, industrial shifts, and ESG considerations, the concentration of critical minerals also engenders serious energy security risks and geopolitical concerns. China’s dominant role as the leading supplier of several critical minerals has fueled apprehensions among advanced economies towards reducing reliance on Chinese supply chains. China controls 28%, 41%, and 78% of the world’s lithium, cobalt, and graphite, respectively. It controls the majority of global processing for many critical minerals and makes most of the parts that go into EV batteries. This positioning has sparked concerns among US officials, who caution that a more rapid energy transition could potentially result in greater dependence on China. The mitigation of risks associated with critical mineral supply chains has thus emerged as a pressing concern in response to both US-China tensions and the increasing demand for clean energy technologies across critical industries.

In this context, friendshoring (or near-shoring) has been identified as a viable approach to address supply chain vulnerabilities. Friendshoring involves building stronger relationships with trusted partners and allies to secure access to critical minerals from multiple sources, thereby reducing dependence on a single source and enhancing supply chain resilience.

It is worth noting that the concept of friendshoring is not confined to critical minerals and can be extended to diverse industries, such as high-tech manufacturing, artificial intelligence, and other sensitive intellectual property sectors that are in the process of decoupling from China. The potential for friendshoring across multiple industries was demonstrated in the remarks made by Aaron Shull, managing director at the Centre for International Governance Innovation, last fall. He stated that the American government’s talks with Canadian miners were “tactically part of a broader strategy” aimed at how Western democracies can confront “adversarial authoritarian state actors,” such as China. Despite various political and legal complexities involved in the implementation of friendshoring policies, initiatives such as the Joint Action Plan on Critical Minerals and the Canada-US Supply Chain Working Group in Canada and the US show promise in the strengthening of a critical mineral value chain between the two nations.

By promoting and facilitating cross-border collaboration on responsible and sustainable practices across the critical mineral value chain, a friendshoring approach can lead to long-term economic benefits for both nations. This approach also aligns with deeply held principles of protecting workers and the social safety net from unfair competition created by coercive societies and “race-to-the-bottom” business practices. Taken together, friendshoring is a promising strategy to promote sustainable growth, mitigate critical mineral supply chain risks, and address geopolitical risks through stronger relationships with trusted partners, ultimately fostering shared economic prosperity amidst global instability.

Canada as a Reliable Partner

Canada’s competitive edge in the critical minerals sector stems from its world-class mineral resource wealth, extensive technology and mining capabilities, and abundant clean energy resources, coupled with its proximity to major markets, stable political and economic environment, transparent legal system, and strong ESG practices. This unique value-added proposition makes Canada a desirable partner for both domestic and international investors and trading partners.

Last year in 2022, there were four key developments related to the critical mineral industry which Canada has the potential to benefit from. First, President Joe Biden invoked Section 303 of the Defense Production Act to secure a supply chain of critical minerals to support the clean energy transition. This invocation allows the White House to provide various incentives to the domestic industry to produce critical minerals necessary for national defense. Second, the Minerals Security Partnership—dubbed a “metallic NATO”—was announced in Toronto, which will work to promote high-ESG production, processing, and recycling of critical minerals to meet the growing demand for clean energy and technology, while simultaneously fostering economic development in participating countries. Third, the Inflation Reduction Act was passed to incentivize investments across North American critical mineral supply chains, with US$500 million to critical minerals processing infrastructure. Fourth, the American Battery Materials Initiative was announced to secure a reliable and sustainable supply of critical minerals essential for power, electricity, and EVs, thereby boosting energy independence, national security, and job creation.

In response to these incentives, the federal government released Canada’s Critical Minerals Strategy, designed to promote responsible sourcing and sustainable production of critical minerals, while also spurring innovation and economic growth within the industry. This strategy, supported by $3.8 billion in Budget 2022, aims to bolster Canada’s chances of capitalizing on the generational opportunity that is the critical minerals sector.

Notably, $1.5 billion of the $3.8 billion has been allocated to the Strategic Innovation Fund (SIF), which will provide support for advanced manufacturing, processing, and recycling applications, facilitating responsible and sustainable production practices across the entire value chain. Furthermore, $40 million has been earmarked to facilitate northern regulatory processes, ensuring that critical minerals projects are subject to rigorous and comprehensive review and permitting processes. An additional $21.5 million has been allocated to support the Critical Minerals Centre of Excellence in developing federal policies and programs, thereby furthering ESG practices across the industry.

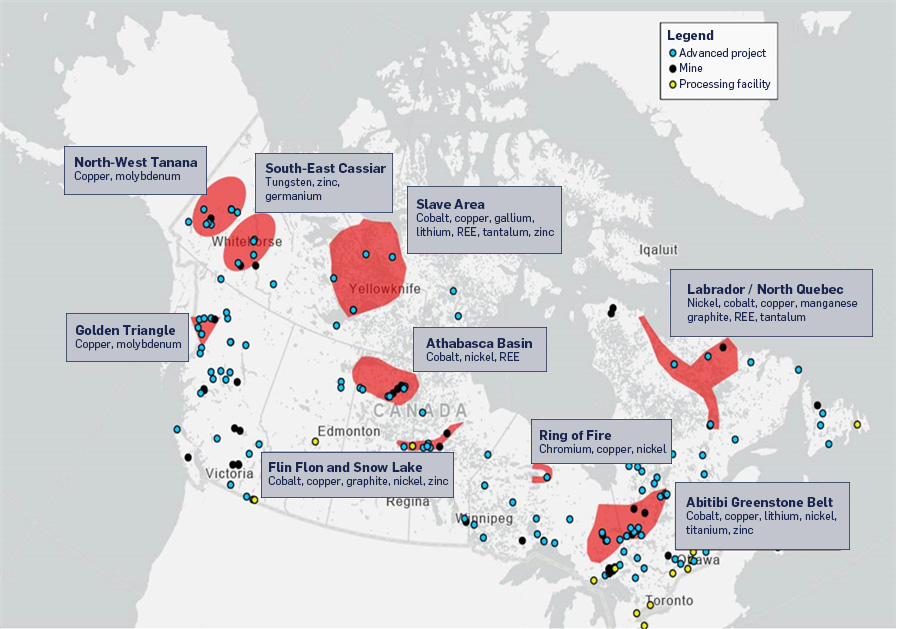

Broadly speaking, Canada has significant mineral resources and contains several regions with high potential for critical minerals production. The diagram below illustrates the eight regions identified by the federal government that have significant potential for critical mineral projects. The federal government plans to further evaluate and prioritize these regions based on their current status, needs, and economic potential before investing substantial resources under the Critical Minerals Strategy.

Figure 1: Regions identified in Canada’s Critical Minerals Strategy deemed to hold potential for critical mineral projects.

Ontario’s Opportunity

Ontario’s current and potential contribution to the Canadian mining industry is significant. Ontario is therefore an important player when considering a future that prioritizes greater friendshoring with the United States. Ontario has an abundance of naturally occurring critical minerals and well-developed mining infrastructure, which is supported by a history of investment by both the government and the private sector. This is further complimented by the integration of Ontario’s mining and EV manufacturing sectors, and by the fact that Ontario is home to Canada’s only producer of cars and trucks and is the only subnational jurisdiction in North America that houses five original equipment manufacturers.

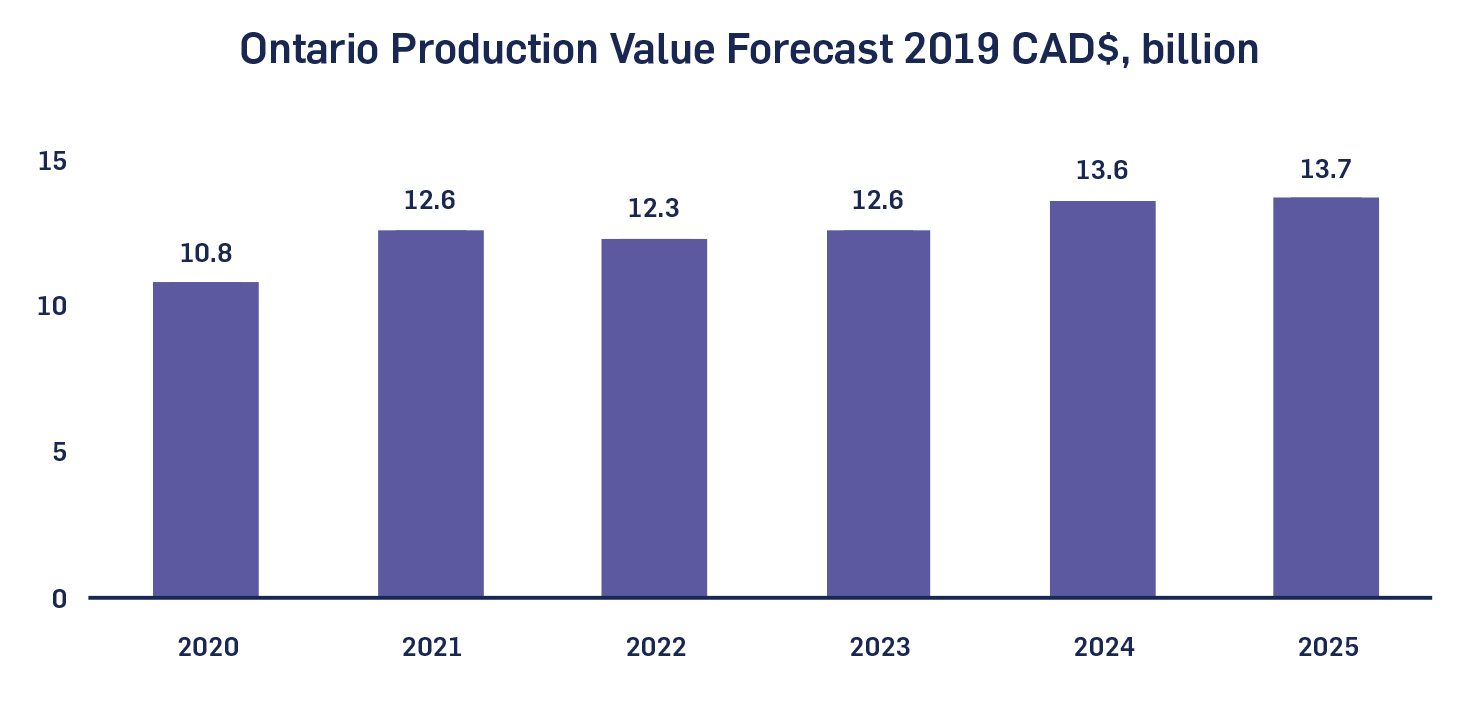

In 2021, Ontario produced $11.1B worth of minerals, which comprised 20% of Canada’s total mineral production. Ontario’s mining operations are expected to grow in coming years, with the province’s total value of mineral production predicted to reach $13.7B by 2025. This expected growth is projected to bring a total contribution of $16.8 billion to the provincial economy, with GDP contribution projected to rise from $7.5 billion in 2019 to $9.3 billion in 2025.

The positive economic impact is expected to have a ripple effect on employment. In Ontario, the mining workforce already includes 75,000 direct and indirect jobs. With increased demand for critical minerals and downstream products, experts forecast labour market pressures in the mining sector, with national estimates suggesting that, by 2025, labour needs will require an additional 30,000 to 48,000 workers over 2021 levels. Similarly, wages and salaries are expected to increase from $3.3 billion to $3.4 billion over the same period. The median weekly mining wage in Ontario was $1,810 in April 2023 compared with $1,090 across all industries. It should be noted that these workers also contribute significantly to the economy, as the average contribution in terms of GDP per Ontario Mining Association (OMA) member employee in 2019 was $337,000, which is approximately three times the average across all industries in Ontario.

Figure 2: Ontario Production Value Forecast, 2019 CAD$, billion. Sources: OMGA Industry Survey, S&P Capital IQ. Adapted from: OMA State of the Ontario Mining Sector.

To realize the potential of Ontario’s critical minerals opportunity, the Province has released its Critical Minerals Strategy (2022-2027) aimed at identifying minerals that hold potential for exploration or development, possess strategic economic importance, support a low-carbon economy, or exhibit global market demand. The strategy aims to enhance the critical minerals sector in Ontario by providing support for mineral exploration and development while strengthening partnerships with Indigenous communities. The strategy also acknowledges the significance of sustainability in the mining industry, with an emphasis on promoting responsible mineral extraction, processing, refining, and recycling through the adoption of best practices for environmental protection, waste management, and mine site rehabilitation. To this end, the strategy seeks to promote the use of clean technologies in the mining industry to minimize overall environmental impact and carbon emissions.

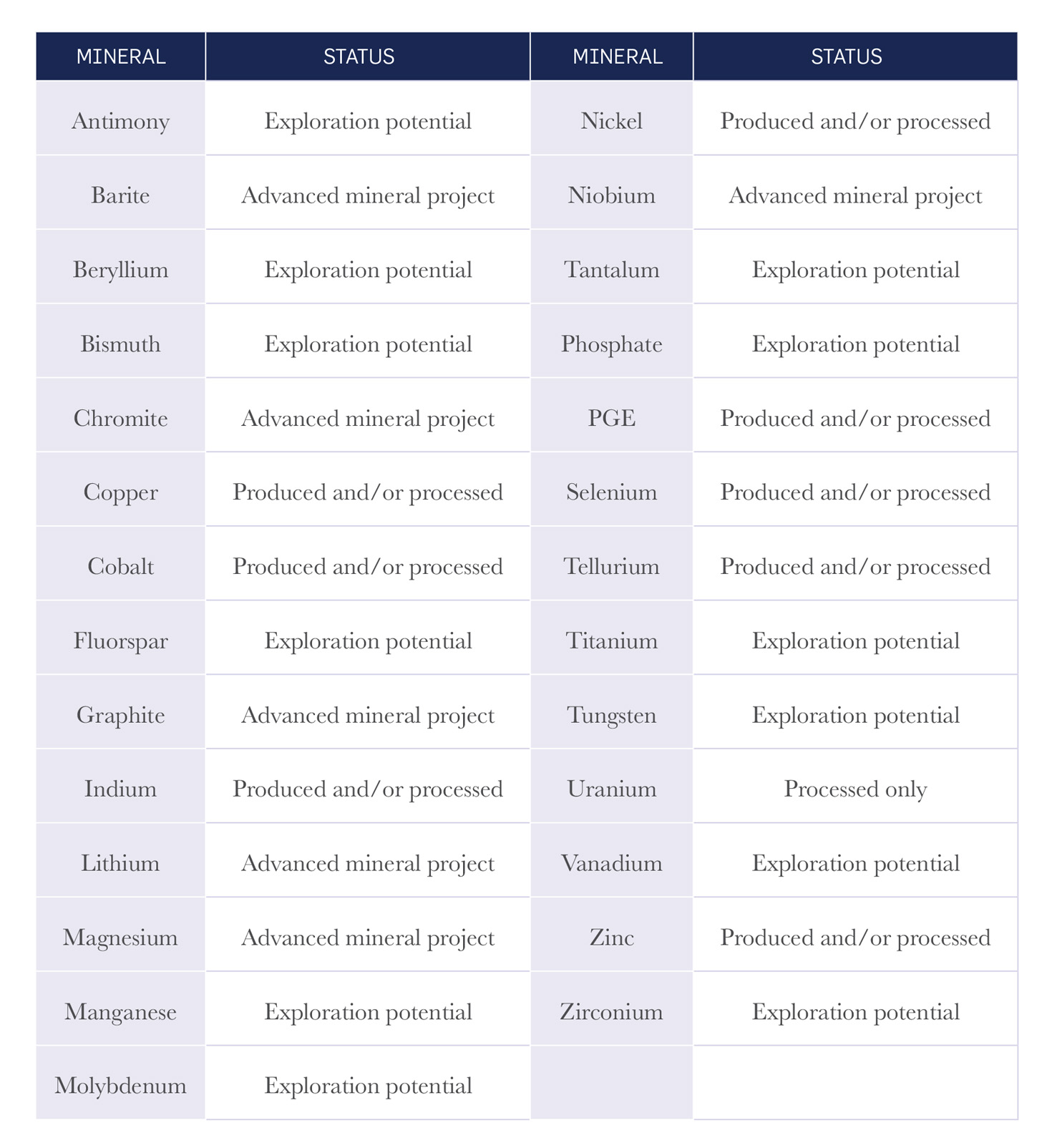

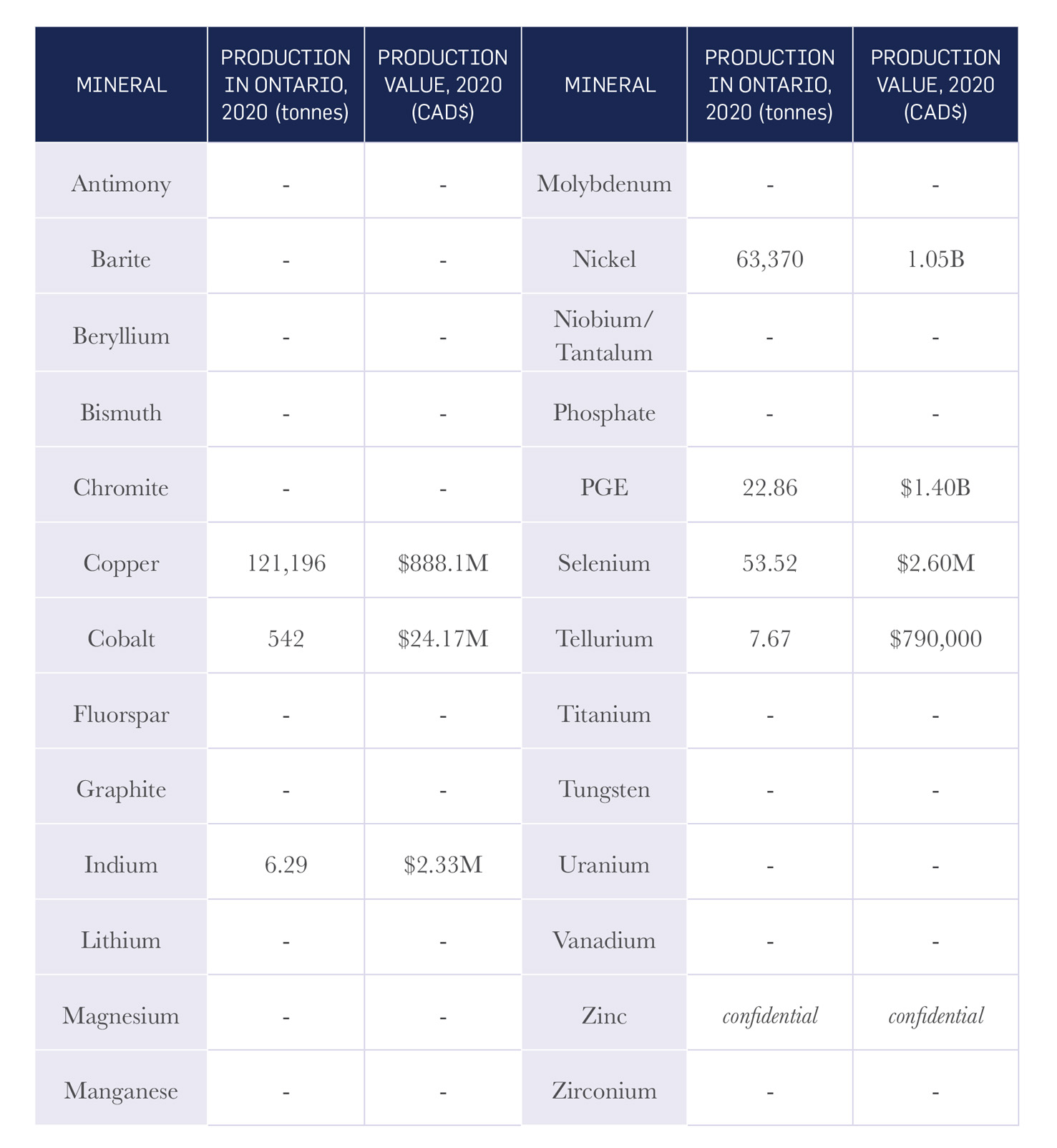

As of March 2022, the province was home to almost 150 critical minerals exploration projects, with 37 active mining operations of which 10 produce critical minerals. The following tables categorize Ontario’s critical minerals by status (Table 1) and quantify their level and value of production (Table 2). It is important to note that, as of 2021, Ontario accounted for more than 50% of the national production of several critical minerals, including indium (100%), platinum-group elements (PGE) (77%), selenium (53%), and tellurium (59%). Ontario also produced 30% of the country’s cobalt, 24% of its copper, and 36% of its nickel. Ontario is also a net exporter of indium, nickel, niobium/tantalum, PGE, selenium, tellurium, uranium, and zinc – except for uranium, each of these critical minerals are used in two or more priority industries in Ontario.

Table 1: Ontario’s Critical Minerals Status as of September 13, 2021. Source: Government of Ontario, Critical minerals framework discussion paper, NRCAN. Adapted from: OMA Critical Mineral Analysis.

Table 2: Ontario’s Critical Minerals Production as of September 13, 2021. Source: Government of Ontario, Critical minerals framework discussion paper, NRCAN. Adapted from: OMA Critical Mineral Analysis.

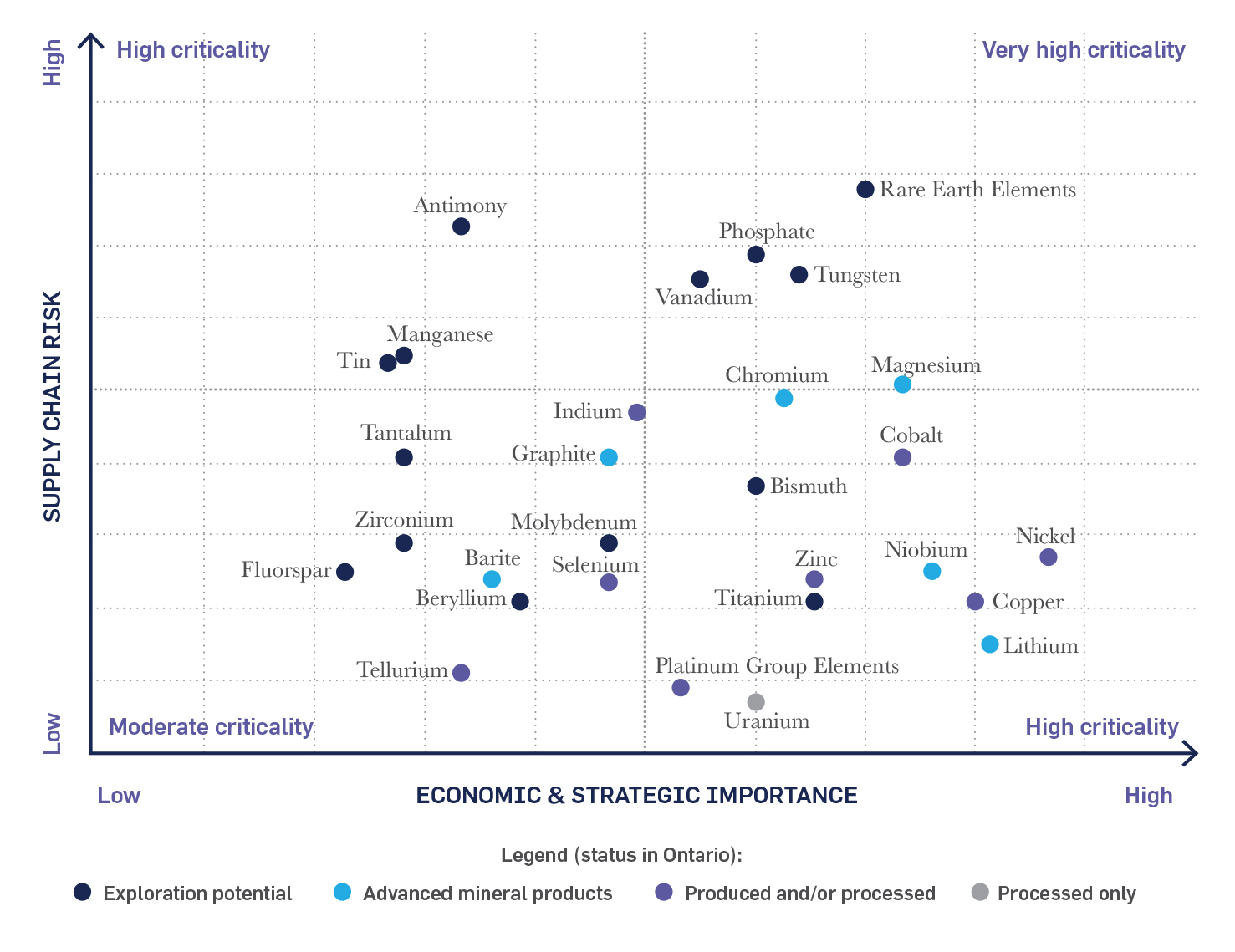

It is worth noting that chromite, indium, manganese, and tungsten are recognized as critical minerals in both Canada and the United States (as per the US Geological Survey) and have relatively low substitutability. Additional analysis on the level of criticality for each mineral is provided in Figure 3 below, which was created by the OMA based on the economic importance and supply chain risk of each critical mineral.

Figure 3: Mineral Criticality Matrix – Economic and strategic importance to the Ontario economy and supply chain risk. Sources: Analysis based on NRCAN, Statistics Canada, USGS and EU data. Note that due to data limitation, cesium is not included. Adapted from: OMA Critical Mineral Analysis.

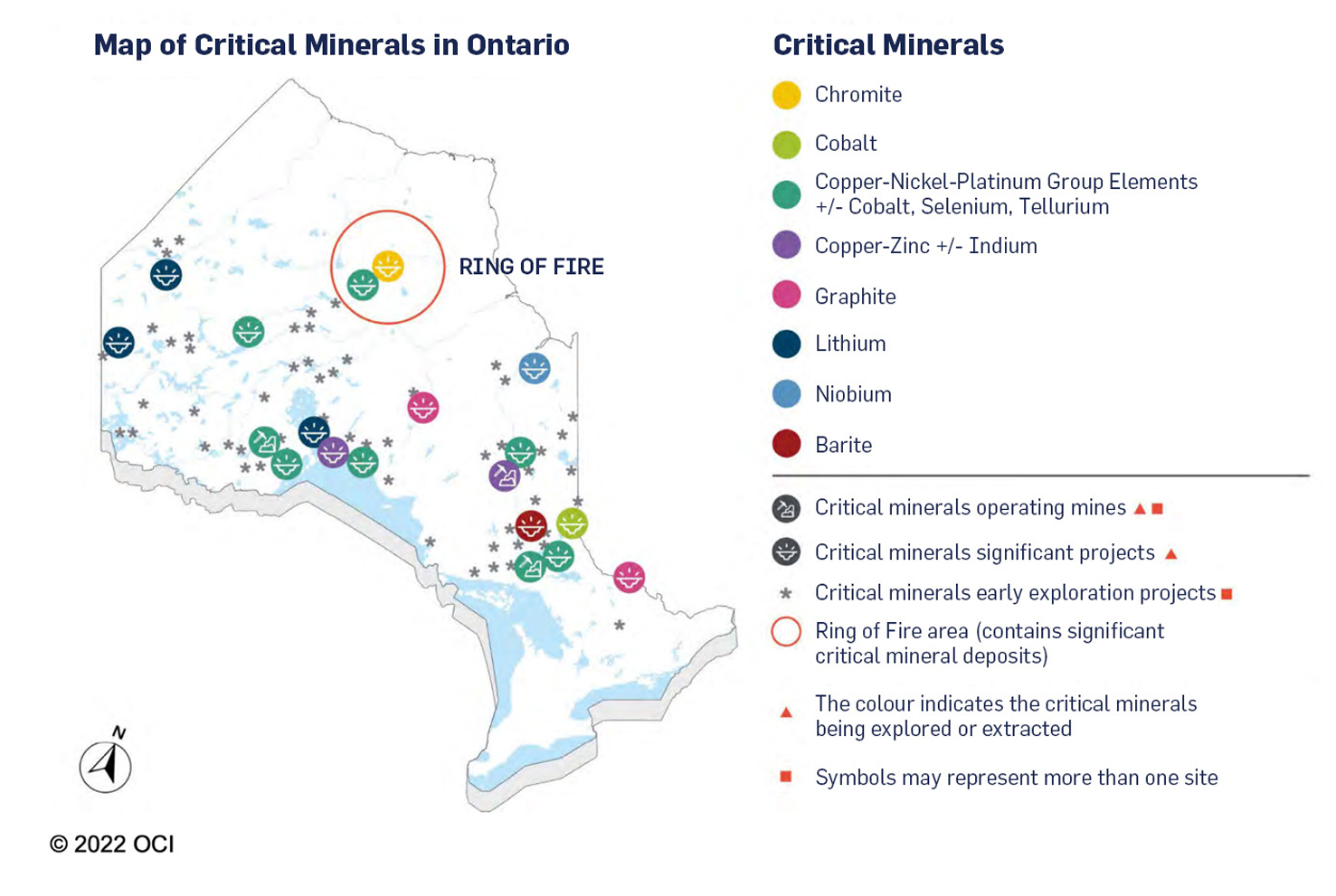

Regarding regional concentration, critical minerals are mined across Ontario’s Northwest, Northeast, South, and Sudbury regions, which include early exploration projects, significant projects, and operating mines (as seen in Figure 4).

Ontario’s Ring of Fire region, located northeast of Thunder Bay and covered by the James Bay Treaty, has garnered significant attention over the past decade for its mining potential. It is roughly 5,000 square kilometers and has various critical minerals, including copper, cobalt, and nickel. Developing this region could help to bolster a domestic supply chain of several critical minerals. However, several steps remain, including securing funding for the access road, addressing environmental and sustainability considerations, and reaching an agreement among actors. Preliminary steps, such as social and environmental impact assessments for a proposed all-season road towards the Ring of Fire, are being led by First Nations in the region. The development of thoughtful, codesigned solutions presents an opportunity to advance reconciliation efforts and create a mutually prosperous relationship.

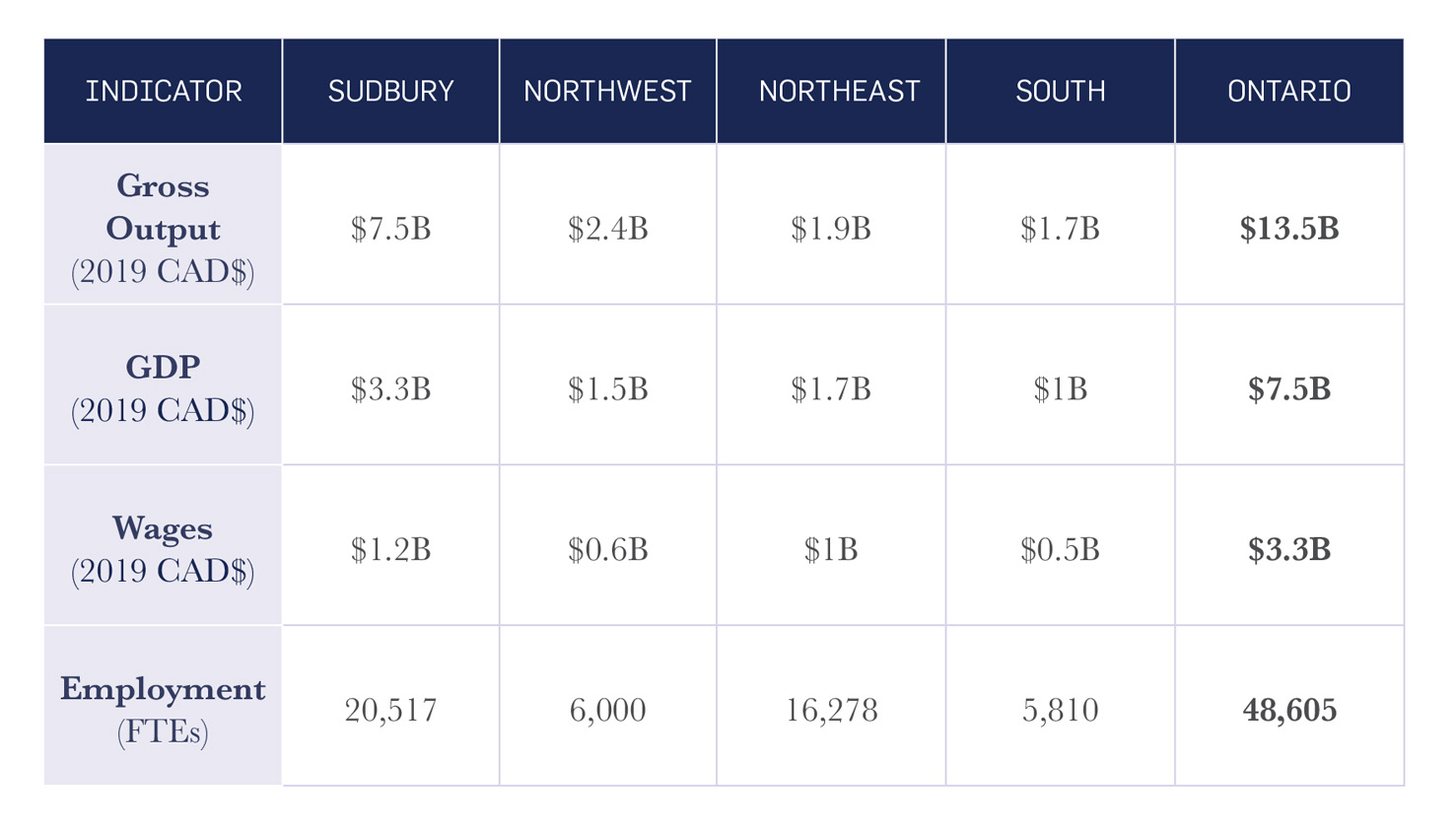

Whereas the Ring of Fire has garnered attention from economists, policy makers, and industry experts for the past decade, the heart of Ontario’s mining operations is currently located in the Sudbury region. Sudbury is home to many of the listed critical minerals in the Canada’s Critical Minerals Strategy and Ontario’s Critical Minerals Strategy and contributed $3.3 billion in GDP to the province in 2019. That year, Sudbury also employed 7,758 workers, roughly 27% of the provincial mining workforce (Table 3).

Figure 4: Overview of critical minerals operating mines, critical minerals significant projects, and critical minerals early exploration projects in Ontario. Source: OVIN Introduction to Critical Minerals: Ontario’s Unique Position

Table 3: Estimated Annual Total Economic Contributions in Ontario’s Regions. Note: Figure displays total of direct, indirect, and induced economic contributions to Ontario’s regional economies. This represents annual contributions based on mineral production in 2019. Sources: OMA Industry Survey, Statistics Canada.

Adapted from: OMA State of the Ontario Mining Sector.

Challenges Facing Ontario

Before Ontario can seize the generational opportunity to develop critical minerals and open the door for future friendshoring with the United States, it must overcome several challenges. These challenges include an anticipated labour shortage, regulatory delays, relationships with First Nations communities, and mid-stream capacity development.

Labour Shortages

Ontario is responsible for a significant portion of the national mining workforce, and it is expected to play a vital role in meeting the anticipated workforce increase in the coming years. However, between October 2022 and April 2023, there has been a decline in the mining workforce of roughly 5,100 workers. Unemployment in the mining sector also reached 9.6% in March 2023, whereas the average across all industries in Ontario was 5%. There is a need to improve both recruitment and retention of workers in the mining sector, while recognizing the opportunities to increase productivity with recent technological advancements.

With most of the mining and quarrying workforce consisting of prime-age workers (age 25 to 54) and older workers (55+), it is clear that the mining industry will rely heavily on new graduates in the future. A 2020 Employer Survey conducted by the Mining Industry Human Resources Council (MiHR) further found that mining employers expected mineral production occupations to experience the highest staff turnover in the future (30%), followed by technical and trades occupations (both at 20%). Finding qualified or skilled workers, retaining employees, and succession planning were the biggest challenges anticipated by most employers in the mining industry.

When looking to the next generation of mining workers, there will need to be a focus on key engineering disciplines that the mining industry relies on. These include mining, geological, and material and metallurgical engineering. Unfortunately, while other engineering programs saw an increase in enrollment between 2015 and 2019, mining engineering programs experienced a roughly one-third decline, which may create challenges in meeting future hiring needs. A diminishing pool of mining engineering graduates could lead to tightness in the labour market, which could hinder future growth.

Concern for tight labour markets in the next generation of mining workers is also seen in the attitudes of younger career seekers towards the mining industry. The least appealing sector among nine different sectors assessed in a 2020 survey conducted by Abacus Data (on behalf of MiHR) was mining. Only 31% of respondents stated they would consider working in mining, while 28% said they probably would not, and 42% stated they definitely would not consider working in mining. Such a finding may limit the incoming talent pipeline and the future growth of the labour pool in the mining industry.

Regulatory Delays

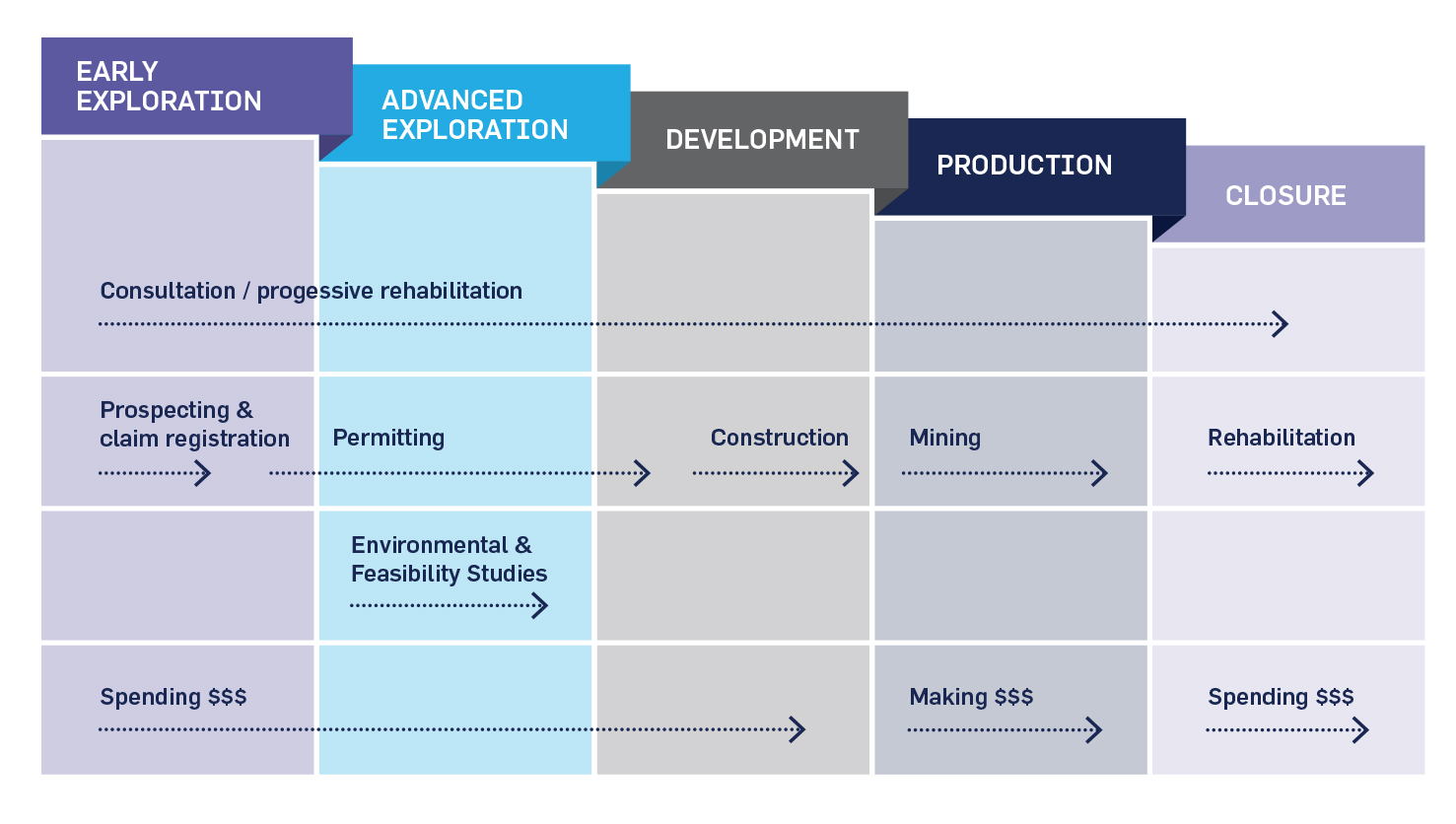

In addition to labour shortages, there have been challenges surrounding regularly processes in the mining sector. Mining projects in Ontario are subject to a comprehensive set of regulations to ensure health, safety, and environmental protection throughout the process, spanning exploration, development, operation, and closure. These regulations encompass the Ontario Mining Act, Environmental Assessment Act, Environmental Protection Act, Ontario Water Resources Act, Public Lands Act, and Occupational Health and Safety Act. Notably, the presence of critical minerals in northern Ontario, where many Indigenous communities are located, triggers a legal duty to consult.

Figure 5: Ontario’s Mining Sequence. Source: Ontario’s Critical Minerals Strategy 2022-2027.

To enhance efficiency and coordination, Ontario offers a streamlined One Window Coordination Process, which clarifies the roles of both project proponents and the government, facilitates efficient project planning, and ensures timely reviews of new mining projects. Despite these efforts, it still takes too long to open mines in the province. A 2021 survey by the Fraser Institute found that, over the last 10 years, 68 percent of mining companies surveyed indicated that the time to permit approval had either lengthened somewhat or lengthened considerably. According to Ontario’s Minister of Mines, MPP George Pirie, it can take between 15 and 17 years to open a mine in the province.

One of the main challenges with Ontario’s Ring of Fire stems from its remote northern location, which results in a lack of essential transportation and electricity transmission infrastructure. To ensure consistent access to the mining operations, approximately 450 kilometers of all-season road must be constructed through boreal forests and swampy peatlands. Additionally, there is currently no existing electricity infrastructure in place. As a result, significant infrastructure projects are required before any mining operations can commence, leading to extended timelines due to both construction and permitting processes.

Tensions with First Nations

Due to the location of many potential critical minerals mining operations on the territories of various First Nations, these communities exert significant influence over mining development projects. This influence is rooted in the legal duty to consult and accommodate Indigenous communities, as well as the incorporation of the United Nations Declaration on the Rights of Indigenous Peoples into Canadian and Ontario legislation. Recognizing and respecting the rights, interests, and aspirations of Indigenous Nations and Peoples through meaningful engagement and consultation is paramount in fostering mining relations based on respect, trust, collaboration, and alignment with sustainable development goals.

If the Ring of Fire, which is located on Treaty 9 territory, is developed appropriately, it could create jobs and economic prosperity for many First Nations in the region. That said, there has been mixed support from First Nations communities, highlighting the complexity surrounding partnerships among the provincial and federal governments and each First Nation.

While the Matawa First Nations, which includes nine communities, have traditionally expressed cautious support for Indigenous-led development in the Ring of Fire region, other First Nations such as Kitchenuhmaykoosib Inninuwug, Wapekeka, Neskantaga, Grassy Narrows, and Muskrat Dam First Nations have voiced strong opposition to development. There is a shared concern that various infrastructure developments, including those mentioned relating to transportation and electricity, could cause environmental damage, loss of wildlife populations, pollution in drinking water, and overall loss of the Indigenous way of life.

Recently proposed amendments to the Mining Act have faced additional opposition from the Matawa Chiefs Council. In an April 2023 news release, the council highlighted a lack of effort to foster meaningful partnerships and reconciliation. In addition, the Neskantaga First Nation has expressed opposition to the proposed road in the Ring of Fire region, citing challenges related to environmental processes and meaningful consultations. In 2021, they filed a legal application questioning their ability to engage in consultations and meet deadlines, citing water-related evacuations and COVID-19 gathering restrictions as contributing factors. The ongoing conflict between the Province and First Nations opposing mining development carries the risk of additional delays or even cancellations for projects that have already experienced significant delays spanning years or even decades.

Mid-Stream Bottlenecks

Despite an abundance of battery materials, Ontario currently lacks the necessary production of key battery-grade minerals like nickel, cobalt, manganese, graphite, and lithium. This is because, to date, the focus has largely been on the upstream (mining) and downstream (battery assembly) stages of the critical mineral value chain. Although efforts are underway to expand North America’s only cobalt sulphate refinery, located in Temiskaming Shores, to include nickel sulphate production, there is an increased need to process critical minerals so that they can be used domestically. Current forecasts show significant supply deficits if midstream and recycling stages of the critical mineral production value chain are not increased. This is especially concerning given that, globally, more than half of manganese (95%), lithium (67%), cobalt (73%), nickel (63%) and graphite (70%) processing and refining capacity is located in China.

By continuing to increase its domestic processing and production capacity, Ontario can capitalize on the high-value stages of the EV battery lifecycle while strengthening a North American supply chain that is less susceptible to risk. Moreover, increased local mineral processing and battery manufacturing capacities would contribute to reducing the carbon footprint of Ontario-made batteries, as international shipping of heavy battery materials generates significant greenhouse gas emissions. By focusing on short-distance domestic transportation, the Province can minimize these emissions and enhance the overall sustainability of its EV battery industry.

Current Efforts by the Province

As outlined in the Ontario Critical Minerals Strategy and other relevant Bills, the provincial government is taking some important steps towards alleviating the labour, regulatory, First Nations, and processing challenges facing the critical minerals industry.

Boosting Labour

Regarding the mining workforce, Ontario’s mining industry has been working to foster an equitable, diverse, and inclusive environment for historically underrepresented groups. In April 2023, the Indigenous share of employment in Ontario was 10.8% compared to 2% across all provincial industries. That said, women only made up 16.1% of the workforce (as opposed to 48% across all industries) while immigrants only made up 5.5% (as opposed to 38% across all industries). Clearly, there are opportunities to enhance participation from traditionally excluded groups and attract skilled workers to the mining sector.

Leveraging immigration and existing programs like the Ontario Immigrant Nominee Program (OINP), the Province aims to further bolster the labour force in the mining industry. In 2021, Ontario also made investments in the Indigenous Workplace Development Program, offering training to Indigenous community members for construction and mining trades. The Skills Development Fund (SDF) adds another $700 million in support for innovative projects that address hiring and training challenges, providing market-driven solutions and support for workers with disabilities. $12 million from the SDF is being invested in people with criminal records to give them a second chance at contributing to the economy and providing for their families.

Ontario has also shown additional support for local employment development, collaboration with the Chiefs of Ontario, improved pathways for foreign workers, and additional opportunities for highly skilled immigrants through the Ontario Bridge Training Program. Many of these supports are included in Bill 79, Working for Workers Act, which includes amendments to several Acts including the Employment Protection for Foreign Nationals Act (2009), Employment Standards Act (2000), Fair Access to Regulated Professions and Compulsory Trades Act (2006), Ministry of Training, Colleges and Universities Act, Occupational Health and Safety Act, Ontario Disability Support Program Act (1997), and Ontario Works Act (1997).

Streamlined Regulatory Systems

In an effort to streamline regulatory processes, Ontario had made several amendments to the Mining Act through Bill 132, Better for People, Smarter for Business Act, and Bill 276, Supporting Recovery and Competitiveness Act. These amendments include the consistent application of the 45-day requirement for a decision on filing or returning submitted closure plans to closure plan amendments, the establishment of a public registry for licenses of occupation, and the implementation of a “permit by rule” model for the sale of bulk samples. The changes are aimed at enhancing the overall regulatory framework, ensuring that regulations are proportionate and efficient based on the scale of each project. Ontario has also modified regulation 240/00 and provided guidance to clarify closure plan requirements, ensuring a gradual, scalable, and proportional approach to mining activities. These changes contribute to a competitive regulatory framework for all minerals, including critical minerals.

Most recently, Bill 71, Building More Mines Act, serves to amend the Mining Act to include changes related to closure plans, recovery permits, and statutory decision-making authorities. These amendments are intended to modernize the competitive regime, reduce regulatory burdens, and provide the Minister of Mining with decision-making authority and delegation flexibility to expedite approval processes. If passed, this would help companies get permits to recover minerals from mine waste, improve closure planning by having more qualified professionals available to certify plans, allow more flexibility in how mines are rehabilitated post-closure, and increase the options for companies to pay financial assurance.

At the intergovernmental level, Ontario recently became the Ninth Jurisdiction to join Canada’s Regional Energy and Resource Tables. The Canada-Ontario Regional Table will work to ensure that regulatory requirements for energy and resource projects across the critical mineral value chain are implemented effectively and in a timely fashion.

Reconciliation Efforts

Regarding economic reconciliation efforts with First Nations, the province has demonstrated its commitment to sharing economic benefits through Resource Revenue Sharing (RRS) agreements. These agreements, currently in place with Grand Council Treaty #3, Wabun Tribal Council, and Mushkegowuk Council, benefit 35 First Nations. Since 2018, over $93 million has been shared from mining tax revenues, royalties, and forestry stumpage revenues. This funding plays a crucial role in enhancing education, healthcare, economic development, and community priorities while strengthening local planning and decision-making. Ontario is working to expand RRS agreements to include more Indigenous communities and to incorporate aggregate royalties as part of the revenue-sharing framework, to ensure Indigenous communities are benefiting more fully from mining development activities.

The Province is also offering $4.7 million in annual support through the Aboriginal Participation Fund to support Indigenous consultation at various stages of mining development, as well as to help engage Indigenous communities in educational activities and build relationships related to mineral exploration and development. This reflects an acknowledgement of the importance of collaborating, information sharing, and facilitating greater Indigenous participation in development and business opportunities in critical minerals supply chains. Furthermore, to strengthen the participation of Indigenous-owned businesses in the critical mineral supply chain, the Ontario government proactively procures goods and services from Indigenous-owned businesses. The Northern Ontario Heritage Fund Corporation (NOHFC) also offers programs that facilitate the delivery of professional services from Indigenous communities to the mining sector.

This past March, as part of a historic partnership, the Ontario government granted approval for a First Nations-led Terms of Reference (ToR), proposed by Webequie First Nation and Marten Falls First Nation. These terms outline construction of the much-needed all-season, multi-use road that will connect the proposed Ring of Fire mining development area to the communities of Webequie and Marten Falls, as well as to the Ontario highway network. The collaborative efforts between Marten Falls and Webequie First Nations, alongside the provincial government, demonstrate a milestone in fostering a cooperative alliance aimed at the planning and realization of the Northern Road Link project.

Processing and Waste-Recovery Capacity

Finally, in recognition of the need to bolster domestic processing and waste recovery, the Province is providing support through programs like the NOHFC. The NOHFC has invested $336,000 in Frontier Lithium’s innovative lithium extraction process and $5 million in Electra Battery Materials in Temiskaming Shores to bolster domestic production of battery-grade cobalt sulfate. Ontario also is investing $250,000 to facilitate establishment of two new battery production lines at the upcoming Battery Materials Park near Cobalt. These production lines, the first of their kind in the province, will play a pivotal role in helping to meet the critical mineral processing demand necessary to support the EV supply chain in North America. Additionally, it was recently announced that the NOHFC is providing $750,000 to accelerate the commercial recovery of critical minerals from mine waste.

Recommendations

In line with current efforts by the provincial government, the following recommendations are offered as opportunities to further advance Ontario’s position as a friendshoring partner in the North American critical minerals value chain. Further context is provided for each recommendation below.

- Implement targeted strategies to attract young people, immigrants, and women to the mining sector, including youth advisory committees, research and career awareness initiatives, and collaboration with student associations.

- Establish mentorship programs and specialized scholarships for underrepresented groups to enhance participation and create a supportive environment.

- Increase funding for the Enhance Your Community Stream of the NOHFC to improve the quality of life in mining communities and promote sustainable growth.

- Strengthen relations with First Nations through co-ownership partnerships and draw insights from successful energy infrastructure projects.

- Expand the eligibility of Ontario’s Aboriginal Loan Guarantee Program to include mining projects, following the example of Alberta’s Alberta Indigenous Opportunities Corporation.

- Identify vulnerable points in the value chain and invest in nickel-sulphate processing and waste recovery capacity.

- Explore the possibility of exporting mine waste to the United States for critical mineral waste recovery, particularly in Michigan.

- Signal continued support for friendshoring principles in the face of potential protectionist measures by collaborating with US states in a joint Canada-US initiative to fund research on enhancing value chain integration and friendshoring practices.

Recruitment & Retention Efforts

To proactively address the existing gap and facilitate a sustainable workforce within Ontario’s mining industry, it is imperative to implement targeted strategies. These strategies should focus on attracting more young people, immigrants, and women to the sector, while also prioritizing funding for community amenities in mining communities.

To attract more young people from universities, efforts should focus on increasing student engagement and changing the perception that mining requires relocation, is dangerous, and is primarily a male profession. Establishment of a youth advisory committee in partnership with the OMA and existing student associations like the Ontario Undergraduate Student Alliance (OUSA) would prove beneficial in providing valuable input and guidance. This committee would actively contribute to the design and implementation of research and career awareness initiatives, while integrating up-to-date labour market information to ensure the effectiveness of these initiatives. Active participation in conferences and networking opportunities within the mining, career development, and education sectors in Ontario would foster collaboration and facilitate valuable connections to enhance the reach and impact of initiatives.

Ensuring representation from underrepresented groups, particularly immigrants and women, would be crucial for the effectiveness of the youth advisory committee. Existing data from MIHR highlights the inadequate representation of these groups in Ontario’s mining workforce, but further data is needed to understand the reasons behind this disparity and capture qualitative information regarding their experiences. Furthermore, the development of enhanced mentorship programs targeted at underrepresented groups is recommended. Leveraging existing resources such as the OINP could facilitate connections between immigrants and mentors within the Ontario mining industry. In terms of gender diversity in mining, it is recommended that the provincial government gather data on the frequency with which mining organizations engage in initiatives such as the MIHR’s Gender Equity in Mining Works (GEM). This would be helpful in determining whether provincial incentives are necessary for greater participation in these types of programs. By prioritizing representation and mentorship, the mining sector can foster a more inclusive and supportive environment for underrepresented groups, which would increase the attractiveness of the mining sector for these workers in the future. Moreover, the establishment of specialized scholarships exclusively designed for women enrolled in mining engineering programs would serve as a dual-purpose measure, acknowledging exceptional academic performance while simultaneously fostering greater female representation within the mining workforce for years to come.

To enhance retention strategies, it is recommended that the provincial government allocate increased funding towards the Enhance Your Community Stream of the NOHFC. This stream plays a vital role in enabling northern municipalities, Indigenous communities, not-for-profit organizations, and Local Services Boards to not only seize economic opportunities but also contribute significantly towards enhancing overall quality of life. By increasing financial support for this program, the government can significantly enhance its impact and promote sustainable growth in these areas by establishing worker-friendly communities with a high quality of life.

First Nations Partnerships

Improved relations with First Nations is crucial for the future of the mining industry in Ontario. This will not only ensure the successful advancement of mining projects with support from key stakeholders but also safeguard the significant contribution of Indigenous employment within the mining workforce.

In alignment with the recently approved First Nations-led ToR for the Northern Road Link project, it is highly advisable that future development projects at various stages within the mining development regulatory process be spearheaded by First Nations communities. Additionally, the provincial government can draw valuable insights from other large-scale energy infrastructure projects across Canada, which have effectively established meaningful and enduring economic partnerships with First Nations communities. Notably, lessons can be learned from liquefied natural gas (LNG) projects on Canada’s West Coast, where the adoption of co-ownership agreements with First Nations communities has yielded increasing success. A significant milestone was reached in March 2023 when the Cedar LNG project became the first Indigenous-majority owned LNG export facility in Canada, with majority ownership vested in the Haisla Nation. Although the Province presently grants royalties to 35 First Nations via Resource Revenue Sharing agreements, adopting a co-ownership approach would elevate this collaboration to a higher level, granting First Nations communities a substantial say in the progress of projects. While co-ownership may not be of interest to every Indigenous group, academic literature suggests points to a desire for economic independence and self-determination. Such co-ownership partnerships would not only serve as a testament to the government’s commitment to mutually beneficial alliances with First Nations communities but also lay the groundwork for long-term, meaningful partnerships.

Building on the imperative to enhance Indigenous partnerships in Ontario’s mining industry, it would be wise to explore a similar approach to economic reconciliation as implemented by the Alberta Indigenous Opportunities Corporation (AIOC). A first-of-its-kind Crown corporation in Canada, the AIOC has successfully facilitated sustainable development and community prosperity by providing Indigenous communities in Alberta with access to capital for major projects in natural resources, agriculture, telecommunications, and transportation sectors.

To address the barrier of accessing capital, the AIOC offers up to $1 billion in loan guarantees, effectively reducing the cost of borrowing for Indigenous groups and making it easier for them to raise capital for investments. These loan guarantees range from a minimum of $20 million to a maximum of $250 million, providing substantial financial support for Indigenous-led projects. By assuming the debt obligation in the event of borrower default, the AIOC enables access to capital, improves lending terms, and enhances the affordability of financing, ensuring that Indigenous communities can bring their projects to fruition.

In addition to loan guarantees, the AIOC recognizes the importance of capacity support in fostering successful partnerships between Indigenous communities, industry, and the government. The AIOC offers discretionary funds to provide technical support on qualified project opportunities. This support includes access to legal, technical, and economic expertise, assisting Indigenous communities in their transition toward becoming long-term strategic partners in the development of natural resources, agriculture, telecommunications, and transportation sectors. By offering a range of support services, the AIOC ensures that Indigenous communities have the necessary resources to navigate complex investment landscapes and maximize the benefits of their projects.

Ontario currently utilizes the Aboriginal Loan Guarantee Program (ALGP) through the Ontario Financing Authority to support Indigenous participation in renewable energy infrastructure and transmission projects. The ALGP provides a Provincial guarantee for loans to Indigenous entities, allowing them to finance a significant portion (typically around 75 percent) of their equity investment in eligible projects. However, to further advance economic reconciliation in Ontario’s mining sector, it would be necessary to expand the program’s eligibility criteria to also include mining projects, following the successful example set by the AIOC. This expansion would not only empower Indigenous communities in the mining industry, promoting economic independence and self-determination, but also reaffirm the government’s dedication to fostering meaningful and enduring partnerships that drive sustainable economic growth in Ontario.

Closing the Value Chain

By making recent investments in nickel-sulphate processing and waste recovery capacity, Ontario is effectively identifying vulnerable points in the value chain that could become bottlenecks in the future. Continued emphasis should be placed on these segments of the value chain, as this not only mitigates potential bottlenecks but also presents opportunities for expanded economic partnerships with private sectors in mining and automotive industries.

In line with these intentions and with the goal of fostering stronger economic ties with the United States, it would be prudent for the provincial government to explore the possibility of exporting mine waste to the United States for critical mineral waste recovery. Michigan, in particular, has emerged as a significant importer of Ontario’s waste and is steadily developing technological capabilities for efficient and sustainable mine waste recovery. An encouraging development this year involved Michigan Technological University securing a $2.5 million grant from the US Department of Energy to undertake a project focused on achieving net-zero emissions while extracting critical minerals from mine tailings in the Upper Peninsula of Michigan and Minnesota.

Canada-US Integration

Great strides have been made in recent years to build friendshoring efforts in North America across a range of industries. However, with the 2024 US election on the horizon, it is possible there will be a shift in the way that industrial policy is framed in the United States. Instead of prioritizing friendshoring, there may be a growing emphasis once again on protectionist measures, winning support from both sides of the political spectrum. This change in approach could potentially lead Canada to consider its own protective measures in response. To mitigate the potential for a backslide in friendshoring momentum, it would be wise for Canada to signal its continued support for the principles of friendshoring in the medium term.

Ontario is strategically positioned to assume a pivotal role in this context. Firstly, Ontario stands out as a prominent participant in the critical minerals value chain across North America. Secondly, the Province maintains close trade and economic ties with key states such as Michigan, Ohio, and Indiana. These interconnected relationships foster robust trade partnerships, particularly in critical minerals and related industries. Thirdly, Southern Ontario boasts the presence of esteemed academic institutions on a global scale.

There is an opportunity for Ontario to collaborate with nearby states to spearhead a joint Canada-US initiative aimed at funding research on enhancing the integration of value chains across critical industries for increased friendshoring. This endeavor would require participation of academic institutions from both countries, working collaboratively with industry partners and related organizations. The initiative would shed light on the necessary steps to unlock the full potential of friendshoring and foster mutually beneficial economic relationships. The initiative would likely involve direct efforts by the provincial ministries of Colleges & Universities and Intergovernmental Affairs, with support from the federal departments of Innovation, Science, and Economic Development, and Global Affairs.

Conclusion

In light of the growing demand for critical minerals driven by the transition to a low-carbon economy, policymakers face the imperative of ensuring a reliable and sustainable supply while addressing social, environmental, and governance considerations. The concentration of critical minerals in specific regions and the risks associated with supply chain vulnerabilities underscore the need for a friendshoring approach. Friendshoring, which involves building stronger relationships with trusted partners, holds the potential to enhance supply chain resilience and reduce dependence on a single source. This approach extends beyond critical minerals and can be applied to diverse industries. By promoting responsible and sustainable practices and fostering cross-border collaboration, friendshoring can lead to long-term economic benefits and address geopolitical risks.

Canada, with its abundant mineral resources, technological capabilities, and commitment to ESG practices, is well-positioned to be a reliable partner in the critical minerals sector. The federal government’s Critical Minerals Strategy and various initiatives demonstrate a strong commitment to capitalize on the opportunities presented by the critical minerals industry. Ontario has major potential in supporting a future that prioritizes friendshoring with the United States, given its significant mineral resources, well-established mining infrastructure, and integration of mining and EV manufacturing sectors.

By implementing the recommendations set out in this paper and by building on existing initiatives, Ontario can strengthen its role in the North American critical minerals value chain and position Ontario as a reliable friendshoring partner, creating economic benefits for Canada and its international partners.

Giancarlo Da-Ré is an alumni of the global affairs program at the University of Toronto’s Munk School of Global Affairs & Public Policy.

For more information about Ontario 360 and its objectives contact:

Sean Speer

Project Co-Director

[email protected]

Drew Fagan

Project Co-Director

[email protected]

on360.ca