30 on 30

Clean Technology – Transition Briefing

Establishing an Ontario Sovereign Wealth Fund to finance clean technology and realize decarbonization

Issue

Much of the public policy debate on climate change is focused on prevention – including the relative strengths and weaknesses of cap-and-trade, carbon taxes, and regulations. This focus on emission abatement is a critical part of any effective climate change policy. But there is also scope for Ontario to be a global leader in the financing of new clean technologies that can replace higher emitting technologies or processes and in turn lower greenhouse gas emissions. The incoming government should take bold action to stimulate greater investment in the clean energy transition. The creation of a new Ontario Sovereign Wealth could help to enable investment in new, transformative technologies.

Overview: stimulating greater investment in the clean technology transition

Stimulating greater investment in the clean energy transition has been a consistent priority for G-7 and G-20 leaders.

Included in the Italian G-7 Chair’s summary from the Energy Ministerial was the following statement on investment in the clean energy transition:

“The Energy Ministers of Canada, France, Germany, Italy, Japan, the United Kingdom, the Secretary of Energy of the United States of America, and the European Commissioner for Climate Action and Energy (Heads of Delegation) stressed that continued investment in the energy sector, in particular in quality energy infrastructure, in upstream development, in low emissions and in low carbon technologies and in energy efficiency, remains critically important for ensuring future energy security and mitigating risks to sustainable growth of global economy.”[1]

In the German G-20 Leaders’ Climate Action and Energy Plan for Growth there was also a recognition of:

“The need to leverage investment in energy generation, energy distribution, transportation, and energy efficiency infrastructure for a reinforcing system of enhanced investment; and achievement of climate change commitments.”[2]

Some jurisdictions – particularly in Europe – have started to take steps to move in this direction. The goal of “decarbonization” (which has been endorsed by the G-7 by 2100[3]) may seem hard to imagine but it is something that Canadian and Ontario policymakers should be thinking about now. The first reason is that there are opportunities to leverage Ontario’s R&D capacity (including its human capital) to pursue new, dynamic technologies that can help achieve to this long-term goal and mitigate the risks of climate change. The second is that Canadian fossil fuel companies are going to need significant capital to decarbonize their operations and redeploy profits to this end. This transition briefing will principally focus on the latter.

The need for reform

What is the global carbon budget? It is a project of the Global Carbon Project, which is an international scientific organization that seeks to quantify global carbon emissions and their causes. The global carbon budget is an annual publication that measures global greenhouse gas emissions.[4] It also provides a regularized update of the magnitude of emissions abatement required to limit warming to 2°C.

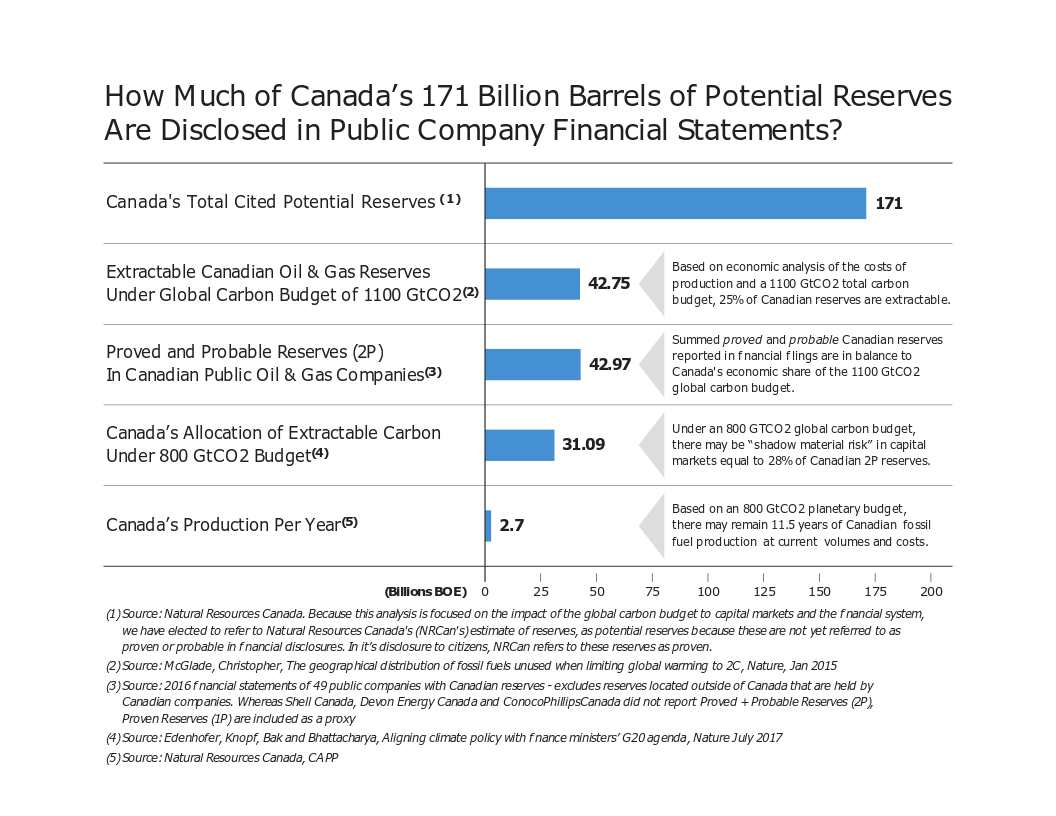

Based on the global carbon budget published in the UN Intergovernmental Panel on Climate Change’s (IPCC) Fifth Assessment Report, a model of global of fossil fuel reserves and extraction was developed and published in the run-up to COP21. This provides an estimate of the compatibility of fossil fuel reserves and extraction and the 2°C target.[5] It concluded that one-third of oil reserves, half of gas reserves and 80 percent of coal reserves cannot be extracted and burned if we are to achieve global targets.

The global carbon budget for this model was capped at 1,100 Gigatonnes (Gt) of GHG emissions from now until 2100. The result of this model for Canada translates as follows: 42.75 billion barrels of oil equivalent (BBOeq) of possible extraction until 2100, which is close to the proved and probable reserves disclosed by 49 Canadian oil & gas companies in June 2017.

Climate scientists are now revising down the global carbon budget consistent with the Paris Agreement, from 600 Gt to 800 Gt. This is now the range of global carbon budgets for, respectively, a 50 percent chance of keeping warming to less than 1.5°C and a 66 percent chance of keeping warming to less than 2°C.[6]

Extrapolating from the global fossil fuel model described above—and based on a 600 or 800 Gt global carbon budget, and the carbon intensity and costs modeled in 2015—the equity value of Canadian publically traded oil & gas companies currently in excess of the global carbon budget runs in the hundreds of billions of dollars. These shares make up a material portion of Canadian public and private pension funds, and these companies are the recipients of billions of dollars of loans from Ontario-based financial institutions, as shown in following table.[7]

There is thus an urgent need to align investment in the Canadian oil & gas industry with the Paris Agreement and the global carbon budget needed to limit warming to 2°C, and to make every effort to limit warming to 1.5°C. Not only is it the right step for our climate but it is also key to minimizing exposure if other countries start to place a greater emphasis on the global carbon budget. This requires, in turn, an alignment between the global financial system and—according to Mark Carney, the former Governor of the Bank of Canada—a quadrupling of investment in sustainable energy and infrastructure.[8]

At the One Planet Summit hosted by French President Emmanuel Macron on the second anniversary of the signing of the Paris Agreement, a global network of sovereign wealth funds was established to accelerate progress on the agreement’s emission goals.

Progress is occurring. The market for green bonds has grown from $500 million in 2008 to $163 billion in 2017. Defining green investment, a focus of the EU Commission in its Action Plan on Financing Sustainable Growth, underpins the EU’s strategy to enable transparency for consumers and savers. The plan was launched by President Macron with the support of 30 EU cities wanting to establish green finance centres.

And these environmental-oriented mandates could come to negatively affect the Ontario-based financial sector. It risks being placed at a disadvantage vis-à-vis its global counterparts whose governments, including the EU Commission, are actively supporting the definition of green financial instruments, and whose central banks are seeking to address system risk posed by climate change and enable greater transparency to citizens.[9]

Ontario’s citizens could start to see below-average returns for their savings as investor confidence in the Ontario financial system is undermined by cumulative, undisclosed carbon-related risks and as Canadian firms fail to maintain the carbon productivity of their global peers.

Remember that the proved and probable reserves for publicly traded companies in Canada’s oil & gas industry are 27 to 45 percent over what global energy models have proposed is Canada’s share of the global carbon budget. All oil-producing and oil-exporting countries face this challenge and will be looking to invest in new value-added uses for oil beyond combustion as a fuel.

And so, if we are to reach the 600 or 800 Gt global carbon budget, Canadian oil & gas companies need to attract significant capital to decarbonize their operations and redeploy profits to this end.

The upshot is that these trends towards decarbonization have huge implications for our financial sector, the fossil fuel industry, and Canada’s leadership on the climate change file.

How to move forward

This is an opportunity and challenge for Ontario. Policymakers must be forward looking here.

The Ontario government can play a leading role that draws on the province’s financial expertise, contributes to global environmental objectives, supports the development of new clean technologies, and ultimately protects against financial risks associated with investments in traditional fossil fuels.

So far, Canada’s financial sector has issued green bonds, mainly for infrastructure and renewable energy but only in limited quantity—even though there is clearly a wider appetite among consumers for these types of investments.

Ontario’s and Canada’s financial sector can and should take a leadership role to decarbonize the oil & gas industry through the development of a market for “emerald bonds”—namely, green bonds targeted at decarbonizing fossil fuel industries and financing alternative higher value products.

In such a market, emerald bonds would be issuable by fossil fuel companies for two purposes: first, to finance the equivalent of 1 to 10 megatonnes of GHG emissions reductions before such measures as methane regulations are put in force; second, to make investments in higher value and zero-carbon assets. Examples of such assets would include renewable energy projects, investments in electricity transmission, sustainable infrastructure (including natural infrastructure) and carbon capture and storage.

One option would be for a newly-created Ontario Sovereign Wealth Fund to recycle a part of the proceeds of carbon auctions to invest in green and emerald bonds. Another would be a one-time capitalization similar to what the federal government is proposing with the Canada Infrastructure Bank.

Over time, the criteria underpinning emerald bonds could shift, and with it the percentage of bond proceeds targeted to emissions reductions versus investments in zero-carbon assets. This shift would be reflective of Canada’s progress when it comes to GHG emissions reductions.

Demand for emerald bonds would come from institutions with an interest in seeing G-7 and G-20 countries meet their Paris Agreement commitments while simultaneously increasing their viability in a post-carbon global economy. Some sovereign wealth funds have specific carve-outs for future investments in fossil fuel companies that they have divested from.

As such, emerald bonds could be used as a means of fostering green investment markets while backing a global “Marshall Plan” to decarbonize fossil fuel companies. These bonds would be issued by companies in all countries with significant fossil fuel investments. Governments could prime the pump for these bonds by providing sovereign backstops. It could ultimately lead to a clean energy transition. And, with some foresight and the right policies, Ontario could help to catalyse it.

Céline Bak is a leader and expert on innovation, climate change and green finance. She addresses global audiences on topics ranging from innovation to climate change, trade and finance. She is President of Analytica Advisors, which tracks the emergence of innovation-based industries